Uninsured motorist coverage helps protect drivers financially after accidents involving uninsured or underinsured drivers. Unfortunately, many drivers do not fully understand how uninsured motorist coverage works until they experience a serious accident themselves.

A car accident can become financially overwhelming in just a few seconds. One moment, you are driving home from work or running everyday errands. However, the next moment, another driver crashes into your vehicle, leaving you with repair bills, medical expenses, insurance paperwork, and unexpected financial stress.

Now imagine discovering that the driver who caused the accident has no insurance coverage at all.

Unfortunately, this situation is far more common across the United States than many drivers realize. In fact, millions of drivers either carry no insurance or only maintain minimum liability coverage that may not fully pay for serious accidents. As a result, even responsible drivers with strong insurance policies can still face major out-of-pocket expenses after a crash.

This is exactly why uninsured motorist coverage is so important.

Uninsured motorist coverage may help cover medical expenses, lost wages, vehicle repairs, and other accident-related financial losses when another driver lacks enough insurance coverage. Additionally, this protection can become extremely valuable after hit-and-run accidents or severe collisions involving underinsured drivers.

Many beginner drivers and first-time insurance buyers overlook uninsured motorist coverage because they assume full coverage insurance automatically protects them in every situation. Unfortunately, that assumption can become extremely expensive after a serious accident.

In this complete guide, you will learn:

• what uninsured motorist coverage actually means

• how uninsured motorist coverage works

• what uninsured motorist coverage may help pay for

• the difference between uninsured and underinsured motorist coverage

• whether uninsured motorist coverage is legally required

• how hit-and-run insurance claims work

• whether full coverage insurance is enough

• how much uninsured motorist coverage drivers should carry

• common uninsured motorist coverage mistakes drivers should avoid

By the end of this article, you will clearly understand how uninsured motorist coverage works and whether this protection makes sense for your financial situation, driving habits, and long-term insurance needs.

Table of Contents

- What Is Uninsured Motorist Coverage?

- Why Uninsured Drivers Are a Serious Financial Risk

- What Does Uninsured Motorist Coverage Cover?

- Uninsured vs. Underinsured Motorist Coverage

- Does Uninsured Motorist Coverage Cover Hit-and-Run Accidents?

- Is Uninsured Motorist Coverage Required?

- Do You Need Uninsured Motorist Coverage If You Have Full Coverage?

- Uninsured Motorist Bodily Injury Coverage Explained

- Uninsured Motorist Property Damage Coverage Explained

- How Much Uninsured Motorist Coverage Should You Carry?

- How Claims Work After an Accident With an Uninsured Driver

- Common Mistakes Drivers Make

- Ways to Save Money Without Removing Important Coverage

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

What Is Uninsured Motorist Coverage?

Uninsured motorist coverage is a type of auto insurance that helps protect you financially if another driver causes an accident but does not have insurance.

In simple terms, this coverage acts as a financial safety net.

Normally, the at-fault driver’s liability insurance should help pay for injuries and damages they caused. But when the other driver has no insurance, recovering compensation becomes much more difficult.

Without uninsured motorist coverage, drivers may face:

- medical bills

- lost wages

- rehabilitation costs

- out-of-pocket repair expenses

- financial stress after serious injuries

This protection becomes especially important because uninsured driving remains a major issue in many parts of the United States.

Even responsible drivers who maintain strong insurance policies themselves can still face financial hardship after accidents involving uninsured motorists.

That is why many financial professionals consider uninsured motorist coverage one of the most valuable optional protections available in modern auto insurance policies.

Why Uninsured Drivers Are a Serious Financial Risk

Many drivers assume most people on the road carry proper insurance.

Unfortunately, that is not always true.

Some drivers intentionally avoid purchasing insurance to save money. Others allow policies to lapse because of financial difficulties.

This creates major risks for everyone sharing the road.

Imagine this situation:

A driver runs a red light and crashes into your vehicle.

You suffer:

- a damaged vehicle

- emergency room bills

- missed work

- ongoing physical therapy expenses

Then you discover the at-fault driver has no insurance.

Without uninsured motorist coverage, recovering compensation can become extremely difficult.

You may need to:

- rely on health insurance

- pay deductibles yourself

- cover lost wages personally

- attempt legal action against a driver who may not have financial resources

Medical costs in the United States are already extremely expensive.

Even relatively moderate injuries may generate:

- ambulance charges

- emergency treatment costs

- imaging scans

- rehabilitation expenses

- specialist appointments

Modern vehicle repairs are also becoming more expensive because cars now contain:

- cameras

- radar systems

- advanced electronics

- lane-assist technology

- safety sensors

One serious accident involving an uninsured driver can quickly create financial problems worth tens of thousands of dollars.

That is why uninsured motorist coverage matters so much.

What Does Uninsured Motorist Coverage Cover?

Coverage details vary depending on your insurer and state laws, but uninsured motorist insurance commonly helps pay for:

- medical expenses

- emergency room treatment

- surgery costs

- rehabilitation expenses

- lost wages

- pain and suffering in some states

- funeral expenses in severe accidents

Some states also offer uninsured motorist property damage coverage, which may help repair your vehicle after accidents involving uninsured drivers.

For example, imagine an uninsured driver rear-ends your car at a stoplight.

You suffer:

- neck injuries

- physical therapy expenses

- emergency medical treatment

- missed income from missing work

Without uninsured motorist bodily injury coverage, many of these expenses may become your responsibility.

This is one reason uninsured motorist coverage can become extremely valuable after serious accidents.

Many drivers mistakenly believe their health insurance alone provides enough protection.

However, health insurance may not cover:

- lost wages

- certain rehabilitation expenses

- deductibles and copays

- long-term financial impact after injuries

Strong uninsured motorist protection may help reduce these financial pressures.

Uninsured vs. Underinsured Motorist Coverage

Many drivers confuse uninsured and underinsured motorist coverage because the names sound similar.

However, they protect against different situations.

Uninsured Motorist Coverage

This applies when the at-fault driver has no insurance at all.

Underinsured Motorist Coverage

This applies when the at-fault driver has insurance, but their coverage limits are too low to fully pay for damages.

For example:

Scenario 1

An uninsured driver causes a serious accident.

They carry no insurance.

Uninsured motorist coverage may help protect you.

Scenario 2

A driver causes a major accident but only carries minimal state-required liability insurance.

Medical bills and damages exceed their policy limits.

Underinsured motorist coverage may help cover remaining eligible costs.

This distinction matters because many state minimum liability limits are relatively low compared to modern medical expenses and vehicle repair costs.

Even insured drivers can still create major financial problems if their policy limits are insufficient after severe accidents.

Does Uninsured Motorist Coverage Cover Hit-and-Run Accidents?

In many states, uninsured motorist coverage may help protect drivers after hit-and-run accidents.

This is extremely important because hit-and-run accidents create unique financial problems.

For example:

- the at-fault driver disappears

- insurance information becomes unavailable

- identifying the responsible driver becomes difficult

Without uninsured motorist protection, drivers may struggle to recover compensation for:

- medical bills

- injury-related expenses

- vehicle damage in some situations

However, claim rules vary between insurers and states.

Some insurers require:

- police reports

- prompt accident reporting

- evidence supporting the hit-and-run event

Drivers should contact law enforcement immediately after hit-and-run accidents whenever possible.

Taking photos, collecting witness information, and documenting the scene carefully may also help support claims later.

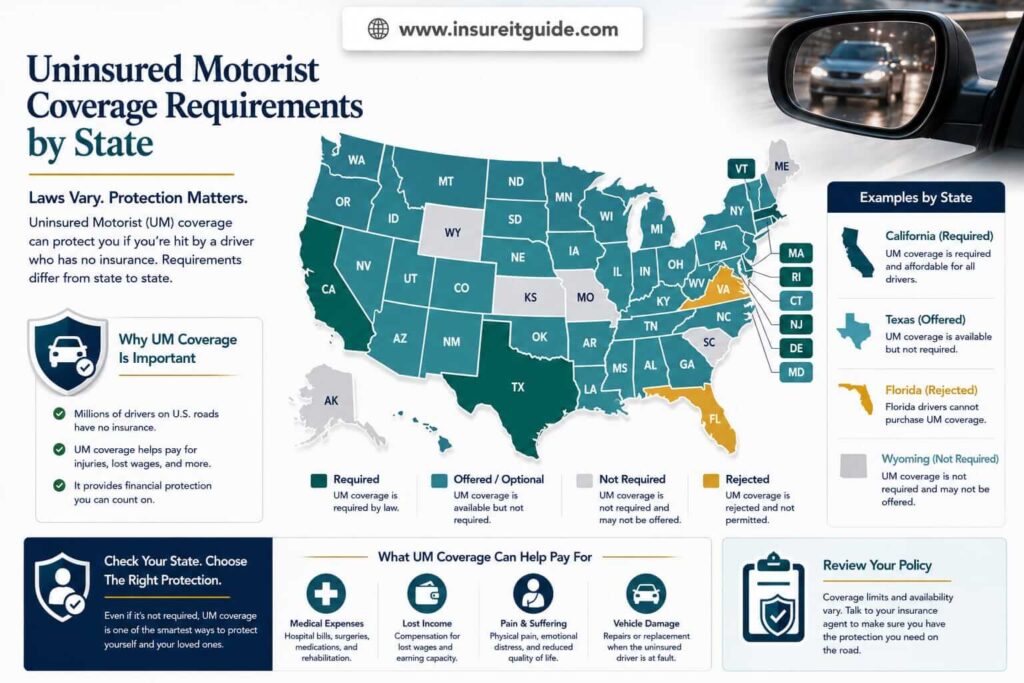

Is Uninsured Motorist Coverage Required?

Requirements vary depending on the state.

Some states require uninsured motorist coverage, while others allow drivers to reject it in writing.

States with higher uninsured driver rates are often more likely to strongly encourage or require this protection.

Even in states where uninsured motorist coverage is optional, many financial experts still recommend carrying it.

Why?

Because state minimum liability laws mainly establish legal minimums—not necessarily ideal financial protection.

Many drivers purchase only minimum coverage because it is cheaper.

Unfortunately, minimum liability limits are often too low after serious accidents involving

- hospital stays

- surgeries

- rehabilitation

- long-term injuries

- expensive vehicle damage

This creates financial risk for everyone sharing the road.

Drivers should not assume state minimum laws automatically provide sufficient financial protection.

Do You Need Uninsured Motorist Coverage If You Have Full Coverage?

This is one of the most misunderstood areas of auto insurance.

Many drivers assume “full coverage” automatically means every type of protection is included.

That is not always true.

Full coverage usually refers to:

- liability insurance

- collision coverage

- comprehensive coverage

However, uninsured motorist protection may still be separate depending on your policy and state laws.

Collision coverage may help repair your vehicle after accidents, but it does not necessarily cover:

- medical bills

- lost wages

- injury-related costs

That is where uninsured motorist bodily injury coverage becomes extremely valuable.

Even drivers with strong full coverage insurance may still benefit significantly from uninsured motorist protection.

One serious accident involving an uninsured driver can create major financial hardship without proper coverage.

Uninsured Motorist Bodily Injury Coverage Explained

Uninsured motorist bodily injury coverage mainly helps pay injury-related costs after accidents involving uninsured drivers.

Coverage may include:

- emergency treatment

- hospital bills

- rehabilitation expenses

- lost wages

- pain and suffering depending on state laws

- funeral expenses in severe cases

This protection becomes especially important after serious accidents causing long-term injuries.

Medical debt can become financially devastating without proper insurance coverage.

Many drivers underestimate how expensive recovery can become after

- surgeries

- physical therapy

- missed work

- long-term rehabilitation

That is why many insurance professionals recommend carrying uninsured motorist bodily injury limits similar to your liability coverage limits.

Uninsured Motorist Property Damage Coverage Explained

Some states offer uninsured motorist property damage coverage.

This protection may help repair your vehicle after accidents involving uninsured drivers.

Coverage rules vary significantly between states.

In some states:

- collision insurance may already cover vehicle damage

- uninsured property damage may include separate deductibles

- availability may differ between insurers

Drivers should carefully review:

- policy wording

- deductibles

- coverage limitations

- state-specific rules

before assuming property damage protection exists automatically.

Vehicle repair costs continue rising every year.

Modern vehicles often require the following:

- specialized labor

- expensive replacement parts

- sensor recalibration

- advanced diagnostics

Even relatively minor accidents can now generate repair bills worth thousands of dollars.

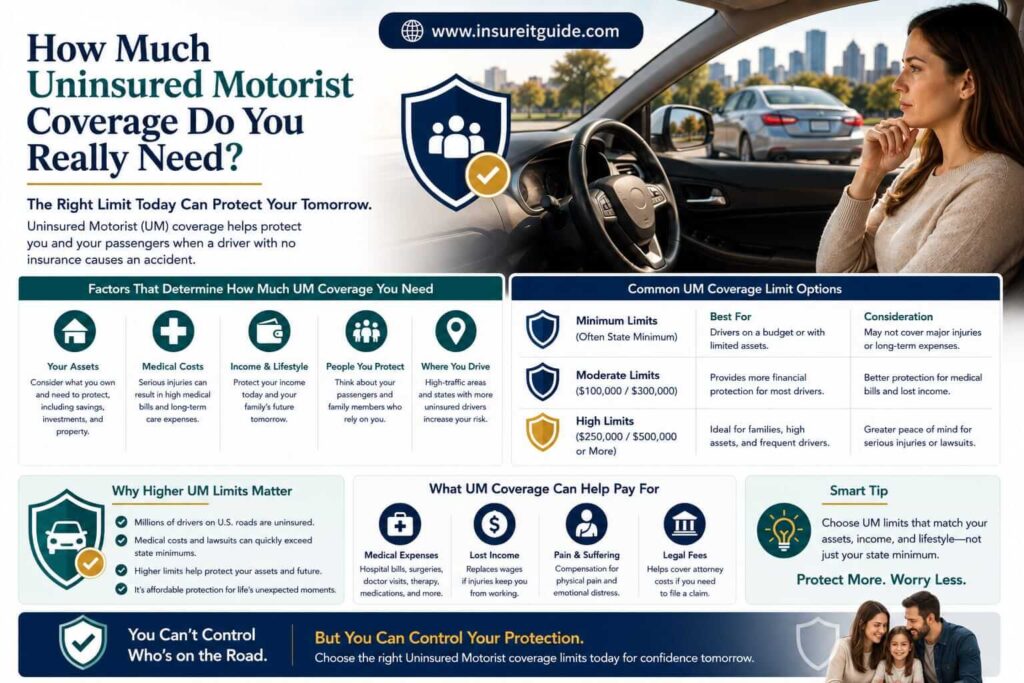

How Much Uninsured Motorist Coverage Should You Carry?

The right amount depends on several factors, including:

- your financial situation

- local uninsured driver rates

- medical cost concerns

- vehicle value

- risk tolerance

Many financial professionals recommend choosing uninsured motorist limits similar to your liability limits.

For example:

- $100,000 bodily injury per person

- $300,000 bodily injury per accident

Higher limits may provide stronger financial protection after severe accidents involving:

- surgeries

- permanent injuries

- extended recovery periods

- expensive medical treatment

Drivers should avoid assuming state minimums provide ideal protection.

Minimum coverage laws are usually designed around legal compliance, not necessarily complete financial security.

The goal of insurance should not simply be meeting legal requirements.

The goal should be protecting your long-term financial stability.

How Claims Work After an Accident With an Uninsured Driver

The claims process after an accident involving an uninsured driver can feel stressful.

Understanding the process ahead of time helps drivers respond more confidently.

Typical steps include:

- Report the accident to law enforcement

- Gather photos and witness information

- Notify your insurance company quickly

- Submit medical records and repair estimates

- Cooperate with claim investigations

- Review settlement details carefully

Insurance companies may investigate:

- fault determination

- accident details

- injuries

- repair estimates

- policy coverage eligibility

Drivers should document everything carefully after accidents.

Helpful evidence may include:

- photos

- police reports

- witness statements

- medical records

- repair estimates

Strong documentation often helps support smoother claim handling.

Common Mistakes Drivers Make

Many drivers accidentally underestimate uninsured motorist risks.

Common mistakes include:

- rejecting coverage to save money

- assuming full coverage includes everything automatically

- choosing very low limits

- ignoring policy reviews

- misunderstanding state-specific rules

Insurance decisions should focus on long-term financial protection rather than only reducing monthly premiums.

One serious accident involving an uninsured driver can create financial stress lasting years without proper coverage.

Drivers should review policies regularly and ask insurers questions whenever coverage details feel unclear.

Ways to Save Money Without Removing Important Coverage

Drivers often want to lower premiums without sacrificing valuable financial protection.

Potential strategies include:

- comparing insurance quotes regularly

- bundling insurance policies

- maintaining clean driving records

- improving credit in eligible states

- choosing appropriate deductibles

- asking insurers about discounts

Removing uninsured motorist coverage simply to reduce monthly premiums may create much larger financial risks later.

Insurance should be viewed as financial protection, not only as a monthly expense.

Saving a small amount each month may not be worth the risk of facing major medical or repair bills after accidents involving uninsured drivers.

Frequently Asked Questions

What happens if an uninsured driver hits my car?

Uninsured motorist coverage may help pay eligible injury-related expenses if an uninsured driver causes an accident.

Does uninsured motorist coverage cover hit-and-run accidents?

In many states, yes. Coverage rules vary depending on policy details and state laws.

Is uninsured motorist coverage required in every state?

No. Some states require it while others allow drivers to reject it in writing.

Do I need uninsured motorist coverage if I have full coverage insurance?

Often yes. Full coverage does not always include uninsured motorist protection automatically.

What is the difference between uninsured and underinsured motorist coverage?

Uninsured coverage applies when the at-fault driver has no insurance. Underinsured coverage applies when their limits are too low to fully cover damages.

Does uninsured motorist coverage cover vehicle damage?

Some states offer uninsured motorist property damage coverage, although rules vary.

Is uninsured motorist coverage worth it?

Many financial professionals consider it valuable because uninsured driving remains common in many parts of the United States.

Key Takeaways

- Uninsured motorist coverage protects drivers after accidents involving uninsured drivers.

- Underinsured motorist coverage helps when the at-fault driver’s limits are insufficient.

- Hit-and-run accidents may qualify under uninsured motorist claims in many states.

- Full coverage insurance does not always automatically include uninsured motorist protection.

- Medical costs and repair expenses continue increasing across the United States.

- Many financial professionals strongly recommend uninsured motorist coverage even when optional.

- Strong insurance protection can help reduce long-term financial risk after serious accidents.

Final Thoughts

Uninsured motorist coverage is one of the most important—and most overlooked—forms of financial protection in modern auto insurance.

Even responsible drivers face risks from:

- uninsured drivers

- underinsured drivers

- hit-and-run accidents

Medical costs and repair expenses continue increasing every year, making strong insurance protection more important than ever.

Choosing uninsured motorist coverage may help protect:

- your savings

- your financial stability

- your long-term recovery after serious accidents

Insurance should never be viewed only as a legal requirement.

It should be viewed as financial protection for your future.

Before rejecting uninsured motorist coverage simply to lower premiums, drivers should carefully consider how expensive even one serious accident could become without proper protection.

For more beginner-friendly insurance guides and educational financial content, visit www.insureitguide.com.