Buying a new vehicle feels exciting.

You drive away from the dealership with a newer car, modern features, and confidence that your auto insurance policy will financially protect you if something goes wrong.

But many drivers discover a major financial problem only after a serious accident or vehicle theft.

Their insurance company may pay significantly less for the vehicle than the amount still owed on the loan.

That remaining balance can become a stressful financial burden, especially when the vehicle is already gone.

This is exactly where gap insurance becomes important. It helps protect drivers financially when a vehicle is totaled or stolen and the remaining loan balance is higher than the vehicle’s actual cash value. Many beginner drivers and first-time car buyers misunderstand how it works.

Some drivers purchase it unnecessarily.

Others reject it without understanding the risks.

And many continue paying for gap insurance long after they no longer need it.

This creates confusion because vehicle loans, insurance settlements, depreciation, and financing structures are not always easy to understand.

In this complete guide, you will learn:

This guide explains what gap insurance is, how it works, what it covers and excludes, when it may be beneficial, and when it might not be necessary. It also explores whether lenders require this insurance, how total loss settlements are handled, how vehicle depreciation can create financial risk, and whether gap insurance is worth the cost.

By the end of this article, you will clearly understand whether gap insurance makes sense for your financial situation and vehicle loan structure.

Table of Contents

- What Is Gap Insurance?

- Why Vehicle Depreciation Creates Financial Risk

- How Gap Insurance Works

- What Does Gap Insurance Cover?

- What Gap Insurance Usually Does NOT Cover

- Gap Insurance for Financed Cars

- Gap Insurance for Leased Vehicles

- When Gap Insurance Makes the Most Sense

- When You Probably Do NOT Need Gap Insurance

- How Gap Insurance Works After a Total Loss Accident

- Is Gap Insurance Required?

- How Much Does Gap Insurance Cost?

- Where Can You Buy Gap Insurance?

- When Should Drivers Remove Gap Insurance?

- Common Mistakes Drivers Make With Gap Insurance

- Is Gap Insurance Worth It?

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

What Is Gap Insurance?

It is a type of optional auto insurance that helps cover the difference between:

- what your vehicle is worth

and - what you still owe on your loan or lease

after a covered total loss.

The word “gap” stands for the financial gap between those two amounts.

This situation usually happens because vehicles depreciate quickly.

The moment a new vehicle leaves the dealership, its market value often begins declining immediately.

Many newer vehicles lose substantial value during the first few years of ownership.

At the same time, vehicle loans may still carry high remaining balances.

Now imagine your car gets the following:

- totaled in an accident

- stolen and never recovered

- severely damaged by flooding

- destroyed in a fire

Your standard auto insurance policy usually pays the vehicle’s actual cash value, not the amount remaining on your loan.

That creates a financial gap.

Gap insurance may help cover that remaining balance. Without it, drivers may still owe thousands of dollars on a vehicle they no longer own. This is why gap insurance can become financially valuable for some drivers.

Why Vehicle Depreciation Creates Financial Risk

Vehicle depreciation is one of the biggest financial realities many drivers underestimate.

Most vehicles lose value quickly during the first few years of ownership.

Some vehicles may lose a significant percentage of their value within the first year alone.

This matters because insurance companies usually base total loss payouts on the following:

- actual cash value

- market value

- depreciation-adjusted replacement value

not on what you originally paid for the vehicle.

Here is a simple example.

You purchase a vehicle for:

$40,000

After one year:

The vehicle’s market value drops to

$31,000

But your remaining loan balance may still be

$36,000

Now imagine the vehicle is totaled in an accident.

Your insurer may pay approximately the following:

$31,000

That leaves a

$5,000 gap

Without gap insurance, you may still owe that amount directly to the lender.

Many drivers do not realize this financial risk exists until after major accidents.

This becomes especially important because newer vehicles often involve the following:

- longer loan terms

- smaller down payments

- higher financing balances

All of these factors increase negative equity risk.

How Gap Insurance Works

Gap insurance only applies in specific situations.

Typically, the process works like this:

- Your vehicle is declared a total loss

- Your auto insurer calculates actual cash value

- Your lender confirms remaining loan balance

- Gap insurance helps cover eligible remaining balances

For example:

Vehicle purchase price:

$42,000

Remaining loan balance:

$37,000

Insurance settlement:

$31,000

Gap insurance may help cover:

$6,000 difference

This protection becomes especially valuable for drivers who:

- financed vehicles with low down payments

- selected long loan terms

- rolled negative equity into newer loans

- purchased vehicles with fast depreciation

Gap insurance mainly protects borrowers from continuing loan obligations after losing the vehicle entirely. However, it is important to understand that it does not replace standard auto insurance.

Drivers still need:

- liability insurance

- collision coverage

- comprehensive coverage

because gap insurance only works alongside qualifying physical damage coverage.

What Does Gap Insurance Cover?

Gap insurance primarily helps cover the difference between:

- the insurance payout and

- the remaining loan or lease balance

after a covered total loss.

This may apply after:

- severe accidents

- vehicle theft

- flood damage

- fire damage

- major weather-related destruction

Gap insurance may help with:

- remaining auto loan balances

- remaining lease balances in qualifying situations

Some policies may also include:

- deductible assistance

- lease deficiency protection

However, coverage details vary significantly between insurers and lenders.

Drivers should always review policy wording carefully.

Gap insurance is most valuable during periods when:

- loan balances remain high

- vehicle depreciation is strongest

This usually occurs during the first few years after purchasing or leasing a vehicle.

What Gap Insurance Usually Does NOT Cover

Many drivers misunderstand gap insurance and assume it covers every financial expense after accidents.

That is not true.

Gap insurance usually does not cover:

- mechanical breakdowns

- engine failures

- overdue loan payments

- late fees

- extended warranties

- routine maintenance

- down payments for replacement vehicles

Gap insurance also generally does not apply to:

- minor repairs

- partial damage claims

- normal depreciation

- cosmetic damage

The vehicle usually must be declared a total loss before gap insurance becomes relevant.

Understanding these limitations is extremely important.

Drivers should never assume gap insurance replaces collision or comprehensive insurance.

Gap Insurance for Financed Cars

Gap insurance becomes especially valuable for financed vehicles.

This is because many borrowers owe more than the vehicle’s actual value during the early years of ownership.

Several factors increase gap risk:

Low Down Payments

Small down payments reduce immediate equity.

Long Loan Terms

72-month and 84-month loans often create slower equity growth.

High Vehicle Depreciation

Some vehicles lose value faster than others.

Rolled Negative Equity

Drivers sometimes include remaining balances from older loans into newer vehicle loans.

This can increase the financial gap dramatically.

For financed vehicles, gap insurance may help protect borrowers from continuing loan obligations after total losses.

Gap Insurance for Leased Vehicles

Gap insurance is also extremely common for leased vehicles.

In fact, many lease agreements already include some form of gap protection.

This matters because leased vehicles often maintain higher payoff balances relative to market value.

If a leased vehicle is totaled, remaining lease obligations may exceed the insurance settlement amount.

Gap insurance may help cover that difference.

Drivers leasing vehicles should:

- review lease agreements carefully

- understand whether gap protection is already included

- avoid purchasing duplicate coverage unnecessarily

Some dealerships attempt to sell additional gap insurance even when lease contracts already include it.

Understanding your lease agreement carefully may help avoid unnecessary expenses.

When Gap Insurance Makes the Most Sense

Gap insurance is usually most valuable when:

- your loan balance is high

- your down payment was small

- your loan term is long

- your vehicle depreciates quickly

- you rolled negative equity into the loan

Drivers purchasing newer vehicles with low down payments are often most exposed to depreciation-related financial gaps.

Gap insurance may also make sense for:

- luxury vehicles

- high-depreciation vehicles

- rapidly financed purchases

- borrowers with minimal emergency savings

For many drivers, gap insurance provides peace of mind during the highest-risk years of vehicle ownership.

When You Probably Do NOT Need Gap Insurance

Not every driver needs gap insurance.

Gap insurance may no longer make financial sense when:

- your loan balance is lower than vehicle value

- you made a large down payment

- your loan term is short

- your vehicle has strong resale value

- you own the vehicle outright

For example, if your remaining loan balance is

$12,000

But your vehicle’s actual cash value is

$18,000

Then there may no longer be a financial gap requiring protection.

Many drivers continue paying for gap insurance longer than necessary simply because they forget to review their policy.

Regularly checking:

- remaining loan balance

- vehicle market value

can help determine whether gap insurance still provides value.

How Gap Insurance Works After a Total Loss Accident

After a severe accident, the insurance company may determine the vehicle is a total loss.

This means repair costs exceed acceptable value thresholds.

The process usually includes:

- Vehicle damage assessment

- Actual cash value calculation

- Loan payoff verification

- Gap insurance review

- Remaining balance settlement

Drivers should:

- notify insurers quickly

- gather documentation carefully

- review settlement details closely

Insurance settlements often depend on:

- depreciation

- vehicle condition

- mileage

- local market value

Gap insurance may help reduce the financial burden created by remaining loan balances after these calculations occur.

Is Gap Insurance Required?

Gap insurance is usually optional.

However, some lenders or lease agreements may require it.

Lenders mainly care about protecting the financial value of the vehicle loan.

Because financed vehicles depreciate quickly, lenders may prefer borrowers maintain gap protection during higher-risk periods.

Even when not required, some drivers voluntarily choose gap insurance for additional financial security.

Drivers should always review:

- financing contracts

- lease agreements

- insurance policy details

to understand whether gap insurance is mandatory.

How Much Does Gap Insurance Cost?

Gap insurance is usually relatively affordable compared to many other auto insurance coverages.

Costs vary depending on:

- vehicle value

- loan structure

- insurer

- lender

- location

Some insurers add gap coverage directly to existing auto insurance policies.

Others sell separate products through:

- dealerships

- lenders

- lease providers

Dealership gap insurance is sometimes significantly more expensive than insurer-provided coverage.

That is why comparing options carefully can help drivers avoid overpaying.

Where Can You Buy Gap Insurance?

Drivers may purchase gap insurance from:

- auto insurance companies

- dealerships

- banks

- credit unions

- lenders

- lease providers

However, prices and terms vary significantly.

Many financial professionals recommend checking insurer pricing before purchasing dealership coverage.

Dealership financing offices sometimes bundle gap insurance into larger financing packages, making it harder for drivers to understand actual costs.

Drivers should always:

- compare pricing

- review terms carefully

- understand cancellation rules

- confirm coverage details

before purchasing gap insurance.

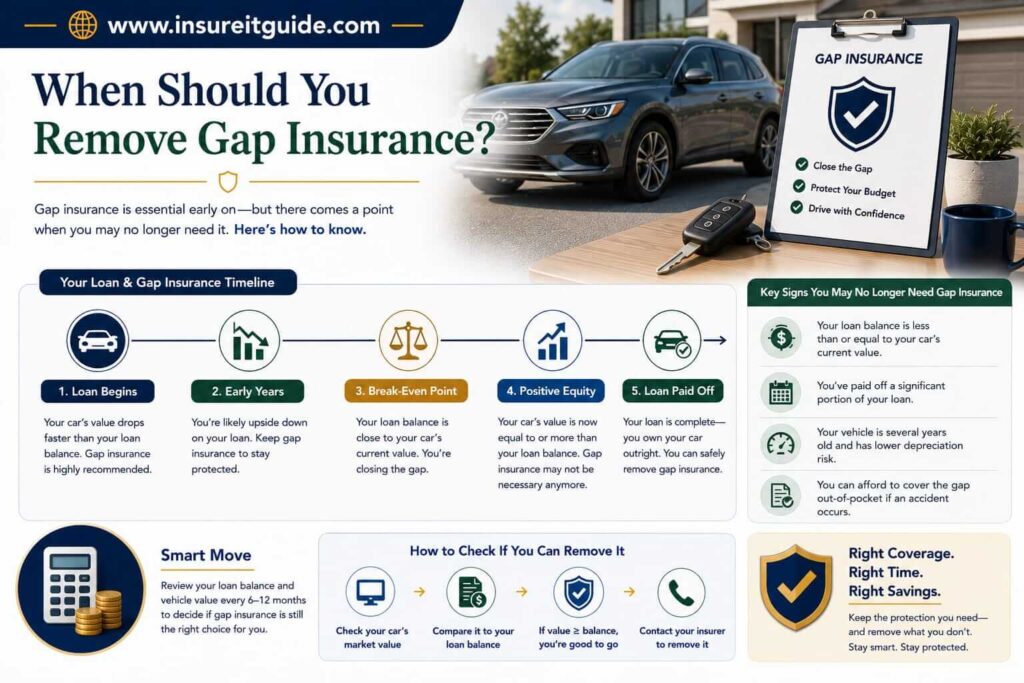

When Should Drivers Remove Gap Insurance?

Gap insurance does not usually need to remain active for the entire loan term.

Drivers should regularly compare:

- remaining loan balance

- vehicle market value

Once the loan balance drops below vehicle value, It may no longer provide meaningful financial benefit.

This often occurs after:

- significant loan repayment

- strong vehicle equity growth

- shorter financing structures

Drivers should review coverage annually to avoid paying unnecessarily for protection they no longer need.

Common Mistakes Drivers Make With Gap Insurance

Many drivers accidentally misunderstand how gap insurance works.

Common mistakes include:

- assuming it covers all repairs

- purchasing duplicate lease coverage

- keeping coverage too long

- ignoring depreciation risk

- focusing only on monthly payment affordability

- misunderstanding total loss settlements

Insurance decisions should focus on long-term financial protection rather than only reducing short-term costs.

One serious total loss accident without proper protection can create major financial stress.

Is Gap Insurance Worth It?

Whether gap insurance is worth it depends on:

- your loan structure

- your down payment

- your vehicle depreciation risk

- your financial situation

For some drivers, gap insurance may provide extremely valuable financial protection.

For others, it may become unnecessary fairly quickly.

Drivers most likely to benefit usually include the following:

- borrowers with low down payments

- long-term auto loans

- high-depreciation vehicles

- minimal savings reserves

Gap insurance is not always essential forever, but during certain periods of vehicle ownership, it can significantly reduce financial risk.

Frequently Asked Questions

What does gap insurance cover?

Gap insurance may help cover the difference between your insurance payout and the remaining loan balance after a total loss.

Is gap insurance required?

Usually no, although some lenders or lease agreements may require it.

Does gap insurance cover repairs?

No. It generally applies only after total losses.

When should I remove gap insurance?

Drivers often remove gap insurance once their loan balance becomes lower than vehicle value.

Is gap insurance worth it for financed cars?

It may be valuable for drivers with low down payments, long loans, or high vehicle depreciation risk.

Key Takeaways

- Gap insurance helps cover remaining loan balances after total losses.

- Vehicle depreciation creates financial risk for financed vehicles.

- It is often valuable during early loan years.

- Full coverage insurance does not eliminate loan balance gaps automatically.

- Drivers should review coverage regularly and remove it when no longer necessary.

- Not every driver needs gap insurance forever.

- Understanding depreciation is critical for smart vehicle financing decisions.

Final Thoughts

Gap insurance is one of the most misunderstood forms of auto insurance protection.

Some drivers purchase it unnecessarily.

Others decline it without understanding the financial risk created by vehicle depreciation.

The key is understanding how:

- loan balances

- vehicle value

- depreciation

- insurance settlements

All work together.

For drivers carrying high loan balances on rapidly depreciating vehicles, gap insurance may provide meaningful financial protection during the riskiest years of ownership.

However, once positive vehicle equity develops, continuing it may no longer make financial sense.

Insurance decisions should always focus on balancing:

- affordability

- financial protection

- long-term financial stability

For more beginner-friendly insurance guides and educational financial content, visit www.insureitguide.com