For many Americans, buying car insurance can feel like learning a completely new language. Terms such as liability coverage, deductibles, policy limits, collision insurance, comprehensive insurance, uninsured motorist coverage, and claims adjusters often appear on quotes and policy documents long before drivers fully understand what they mean.

As a result, many people walk into an insurance office, call an agent, or compare quotes online with one simple request:

“I just want full coverage.”

The challenge is that full coverage car insurance is not actually an official insurance product.

Many drivers are surprised to learn this.

Unlike liability insurance or collision coverage, “full coverage” is not a policy type defined by insurance companies or state regulators. Instead, it is an industry shorthand used to describe a collection of coverages that provide broader protection than a basic state-minimum policy.

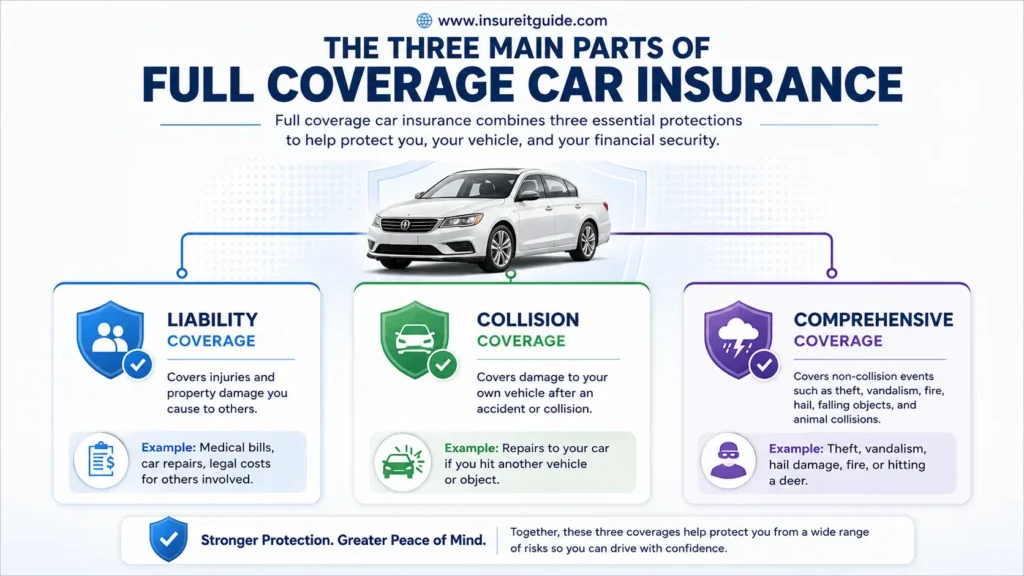

In most cases, full coverage insurance includes:

- Liability Coverage

- Collision Coverage

- Comprehensive Coverage

Together, these coverages help protect drivers against some of the largest financial risks associated with owning and operating a vehicle.

However, one of the biggest misconceptions in auto insurance is believing that “full coverage” means everything is covered.

It doesn’t.

Even the most robust full coverage policy contains limits, exclusions, deductibles, and situations where claims may not be paid. Understanding what is not covered can be just as important as understanding what is covered.

Many claim disputes occur because drivers assume a loss is covered without carefully reviewing their policy details. That’s why learning how full coverage insurance actually works can save both money and frustration later.

Table of Contents

- What Is Full Coverage Car Insurance?

- Why Full Coverage Matters More Than Most Drivers Realize?

- Why So Many Drivers Misunderstand Full Coverage?

- Common Myth: Full Coverage Covers Everything

- What Does Full Coverage Car Insurance Cover?

- Coverages Commonly Included in Full Coverage Car Insurance

- Liability Coverage Explained

- Collision Coverage Explained

- Why Collision Coverage Matters More Today

- Comprehensive Coverage Explained

- Full Coverage vs Minimum Coverage

- What Is Minimum Coverage?

- Full Coverage vs Minimum Coverage Car Insurance

- Full Coverage vs Liability-Only Insurance

- What Full Coverage Does Not Cover

- Full Coverage Insurance Deductibles Explained

- How Much Does Full Coverage Car Insurance Cost?

- How to Find Affordable Full Coverage Insurance

- Is Full Coverage Car Insurance Worth It?

- When Should You Drop Full Coverage Insurance?

- Common Myths About Full Coverage Insurance

- Frequently Asked Questions

- Key Takeaways

- Conclusion

Why Full Coverage Matters More Than Most Drivers Realize

It’s easy to think of insurance as something you buy because the law requires it.

In reality, the financial impact of an accident often becomes clear only when something goes wrong.

Imagine you’ve recently financed a new SUV worth $35,000.

A few months later, you’re driving home from work during a heavy rainstorm. Visibility drops, the road becomes slick, and your vehicle hydroplanes into a guardrail.

The repair estimate comes back at $12,000.

If you carry only state-minimum liability insurance, your insurer may not contribute anything toward repairing your vehicle because liability coverage generally protects other people and their property, not your own car.

That means the entire repair bill could come directly out of your pocket.

Now imagine the exact same accident with full coverage insurance.

After your deductible is applied, collision coverage may help pay for most of the repair costs, potentially saving you thousands of dollars.

This is why understanding full coverage insurance is not just an academic exercise.

It has real-world consequences.

For many households, an unexpected repair bill arrives at the worst possible time. Mortgage payments, rent, groceries, utility bills, childcare expenses, and everyday living costs already consume much of the monthly budget. A sudden $8,000 or $12,000 repair bill can quickly become a financial crisis.

Full coverage insurance helps reduce that risk.

Rather than protecting only against legal liability, it can help preserve your savings when a covered accident, theft, or weather-related event damages your vehicle.

Common Consumer Mistake

Many drivers focus exclusively on monthly premium costs while ignoring potential repair expenses.

Saving $40 or $50 per month by reducing coverage may seem attractive until a major accident leaves you responsible for thousands of dollars in repairs.

A better question is:

If your vehicle were seriously damaged tomorrow, could you comfortably afford to repair or replace it yourself?

If the answer is no, full coverage may provide valuable financial protection.

Why So Many Drivers Misunderstand Full Coverage

One reason full coverage creates so much confusion is that people use the term differently.

Insurance agents use it.

Car dealerships use it.

Lenders use it.

Consumers use it.

Yet there is no single universal definition.

A lender financing your vehicle may require:

- Liability coverage

- Collision coverage

- Comprehensive coverage

An insurance agent may recommend adding:

- Uninsured motorist coverage

- Rental reimbursement

- Roadside assistance

A dealership may simply tell you that the lender requires “full coverage.”

All three parties may be talking about slightly different levels of protection.

As a result, two drivers can both claim they have full coverage while carrying very different policies.

For example:

Driver A

Carries:

- State minimum liability limits

- Collision coverage

- Comprehensive coverage

Driver B

Carries:

- $250,000 bodily injury liability limits

- $500,000 property damage limits

- Collision coverage

- Comprehensive coverage

- Uninsured motorist coverage

- Rental reimbursement

- Roadside assistance

Technically, both drivers might describe their policies as full coverage.

Yet Driver B has substantially broader protection.

This misunderstanding often surfaces after a claim.

A driver may discover that a loss they assumed would be covered actually falls outside the policy’s protections. The issue is not always bad insurance. More often, it is a misunderstanding of what the policy actually includes.

One of the smartest things any vehicle owner can do is review the declarations page and understand exactly what coverages, limits, and deductibles are listed.

Common Myth #1: Full Coverage Covers Everything

This is probably the most common auto insurance myth in America.

Many drivers hear the phrase “full coverage” and assume it means complete protection against every possible problem involving their vehicle.

Unfortunately, that is not how insurance works.

Even comprehensive full coverage policies contain limitations.

For example, most policies generally do not cover:

- Routine maintenance

- Oil changes

- Brake replacement

- Tire wear

- Mechanical breakdowns caused by age

- Engine failure from normal wear and tear

- Personal belongings stolen from the vehicle

- Intentional damage

- Racing activities

A useful way to think about insurance is this:

Insurance is designed to protect against sudden and accidental losses.

It is not intended to function as a maintenance plan, service contract, or vehicle warranty.

Many drivers are surprised when a claim is denied for something they assumed was covered. In reality, the denial often results from a misunderstanding of the policy rather than an error by the insurer.

The more familiar you become with your policy’s exclusions, the less likely you are to encounter unpleasant surprises during the claims process.

What Does Full Coverage Car Insurance Cover?

When people ask:

“What does full coverage car insurance cover?”

they are usually referring to three primary protections:

| Coverage Type | Purpose |

| Liability Coverage | Pays for damage you cause to others |

| Collision Coverage | Pays for damage to your own vehicle after an accident |

| Comprehensive Coverage | Pays for non-collision losses such as theft, vandalism, hail, fire, and falling objects |

Together, these coverages help reduce your financial exposure to many of the risks drivers face every day.

Each coverage serves a different purpose, and understanding the difference is essential when evaluating your policy.

| Liability Coverage | Collision Coverage | Comprehensive Coverage |

| Covers injuries and property damage you cause to others. | Covers damage to your vehicle after an accident or collision. | Covers non-collision events such as theft, vandalism, hail, fire, falling objects, and animal collisions. |

Coverages Commonly Included in Full Coverage Car Insurance

| Coverage Type | What It Helps Cover | Commonly Included in Full Coverage? |

| Liability Coverage | Injuries and property damage you cause to others | Yes |

| Collision Coverage | Damage to your own vehicle after an accident | Yes |

| Comprehensive Coverage | Theft, vandalism, fire, hail, falling objects, and animal collisions | Yes |

| Uninsured Motorist Coverage | Damages caused by uninsured or underinsured drivers | Varies by state/Optional |

| Rental Reimbursement | Temporary transportation expenses after a covered claim | Optional |

| Roadside Assistance | Towing, jump-starts, lockouts, and emergency roadside assistance | Optional |

Liability Coverage Explained

Liability insurance forms the foundation of nearly every auto insurance policy in the United States.

In most states, it is legally required.

Liability coverage primarily protects other people when you cause an accident.

It generally consists of two parts:

Bodily Injury Liability

This may help pay for:

- Medical bills

- Hospital expenses

- Rehabilitation costs

- Lost wages

- Legal settlements

- Pain and suffering claims

for individuals injured in an accident you caused.

Property Damage Liability

This may help pay for:

- Vehicle repairs

- Fences

- Buildings

- Utility poles

- Mailboxes

- Other damaged property

caused by an at-fault accident.

Many drivers focus heavily on protecting their own vehicles while overlooking the importance of liability limits.

In reality, liability coverage often provides the most important financial protection in the entire policy.

A serious accident involving injuries can quickly generate claims worth tens or even hundreds of thousands of dollars.

Without adequate liability limits, your personal assets may be exposed to significant risk.

Real-Life Example

Imagine you’re driving home after picking up groceries.

Traffic suddenly stops ahead.

You brake, but not quickly enough, and rear-end the vehicle in front of you.

The other driver suffers neck injuries and requires medical treatment.

The resulting costs include:

- Medical expenses: $15,000

- Vehicle repairs: $8,000

Your liability coverage may help pay these costs up to your policy limits.

However, it generally will not pay to repair your own vehicle.

That is where collision coverage becomes important.

Many insurance professionals recommend carrying liability limits above state minimum requirements because minimum limits often provide less protection than drivers realize.

A major accident involving multiple vehicles or serious injuries can exceed minimum coverage surprisingly quickly.

Collision Coverage Explained

Collision coverage helps pay for damage to your own vehicle after an accident.

Unlike liability insurance, which protects other people and their property, collision insurance focuses on your vehicle.

This is one of the most valuable parts of a full coverage policy because vehicle repairs have become dramatically more expensive over the past decade.

Today, even a seemingly minor accident can lead to a surprisingly large repair bill.

Collision coverage commonly applies to situations involving:

- Rear-end accidents

- Single-vehicle crashes

- Rollovers

- Hitting a guardrail

- Hitting a tree

- Vehicle-to-vehicle collisions

- Striking a utility pole

- Certain parking lot accidents

Many drivers mistakenly believe collision coverage only applies when another vehicle is involved.

In reality, collision coverage generally applies whenever your vehicle collides with another object, regardless of fault.

If you slide into a guardrail during a snowstorm or accidentally hit a concrete pillar while parking, collision coverage may help pay for repairs, subject to your deductible and policy terms.

Why Collision Coverage Matters More Today

Many consumers underestimate modern repair costs.

Vehicles today contain far more technology than they did even ten years ago.

Modern vehicles often include:

- Backup cameras

- Blind-spot monitoring systems

- Radar sensors

- Lane departure systems

- Adaptive cruise control technology

- Parking assistance systems

As a result, a damaged bumper may no longer be “just a bumper.”

What appears to be a minor repair may involve recalibrating sensors, replacing electronic components, and performing advanced diagnostics.

A repair bill can quickly climb into the thousands.

Common Consumer Mistake

Many drivers assume:

“My vehicle isn’t new anymore, so collision coverage isn’t worth it.”

But vehicle age alone rarely tells the whole story.

A better question is:

“Could I comfortably pay for major repairs tomorrow without disrupting my finances?”

If the answer is no, collision coverage may still provide significant value.

Example: Collision Claim

Imagine you’re backing out of a crowded grocery store parking lot on a Saturday afternoon.

You glance over your shoulder, but a concrete pillar sits in a blind spot.

You hear the impact immediately.

Repair estimate:

$4,800

Deductible:

$500

Insurance payment:

$4,300

Instead of paying nearly five thousand dollars yourself, your out-of-pocket expense is limited to the deductible.

For many households, that difference can be substantial.

What This Means for Drivers

Collision coverage is often most valuable when:

- Your vehicle still has meaningful value.

- You have a loan or lease.

- Major repair costs would create financial stress.

- You rely heavily on your vehicle for work, school, or family responsibilities.

If replacing or repairing your vehicle would significantly impact your finances, collision coverage deserves serious consideration.

Full Coverage vs Minimum Coverage Car Insurance

| Feature | Minimum Coverage | Full Coverage |

| Meets state legal requirements | Yes | Yes |

| Includes liability coverage | Yes | Yes |

| Covers damage to your own car after an accident | No | Yes, through collision coverage |

| Covers theft | No | Yes, through comprehensive coverage |

| Covers hail, fire, vandalism, and falling objects | No | Yes, through comprehensive coverage |

| Usually required by lenders or leasing companies | No | Yes |

| Monthly premium | Lower | Higher |

| Financial protection after vehicle damage | Limited | Broader |

Comprehensive Coverage Explained

Comprehensive insurance protects against many risks that occur when your vehicle is not involved in a traditional collision.

Many drivers don’t fully appreciate comprehensive coverage until they need it.

Unlike collision coverage, which focuses on impacts and crashes, comprehensive coverage helps protect against unexpected events that are often beyond your control.

Common covered events may include:

- Theft

- Vandalism

- Fire

- Flooding

- Hail damage

- Falling objects

- Windstorms

- Animal collisions

For many drivers, comprehensive coverage provides protection against risks they rarely think about until something happens.

Example: Vehicle Theft

Imagine you finish grocery shopping on a Saturday afternoon.

You return to the parking lot.

Your vehicle is gone.

The theft creates more than just financial stress.

Suddenly you may be without transportation for:

- Work

- School drop-offs

- Medical appointments

- Family errands

If the vehicle is never recovered, comprehensive coverage may compensate you for its actual cash value, minus the deductible.

Without comprehensive coverage, the financial loss could fall entirely on you.

Example: Deer Collision

Many drivers are surprised by this one.

Suppose you’re driving home on a dark rural highway.

A deer suddenly runs across the road.

You collide with it.

Damage estimate:

$7,500

Many consumers assume this falls under collision coverage.

In most cases, striking an animal is generally considered a comprehensive claim.

This distinction frequently surprises drivers during the claims process.

Example: Hail Damage

Imagine waking up after a severe overnight hailstorm.

You step outside and discover dozens of dents across:

- The hood

- Roof

- Doors

- Trunk

Repair estimate:

$6,500

Without comprehensive coverage, you could be responsible for the entire amount.

With comprehensive coverage, your insurer may help pay for repairs after the deductible is applied.

Common Consumer Mistake

Many people assume comprehensive coverage only protects against theft.

In reality, theft represents just one part of the protection.

Weather-related claims, animal collisions, vandalism, and falling objects often generate substantial comprehensive claims every year.

What This Means for Drivers

Comprehensive coverage is often especially valuable when:

- Your vehicle has significant value.

- You live in an area prone to severe weather.

- Vehicle theft is common in your area.

- You regularly park outdoors.

- Replacing the vehicle would be financially difficult.

For many drivers, comprehensive coverage provides protection against risks they simply cannot predict or control.

Full Coverage vs Minimum Coverage

One of the most important decisions drivers make is choosing between minimum coverage and full coverage.

At first glance, the decision may seem straightforward.

Minimum coverage usually costs less.

Full coverage usually costs more.

However, the true difference becomes clear after a claim occurs.

What Is Minimum Coverage?

Minimum coverage refers to the least amount of insurance required by your state.

In most states, this consists primarily of liability coverage.

For example, a state may require:

- $25,000 bodily injury liability per person

- $50,000 bodily injury liability per accident

- $25,000 property damage liability

These limits help pay for damage you cause to others.

However, they generally do not help pay for damage to your own vehicle.

Comparing Protection Levels

| Coverage Type | Minimum Coverage | Full Coverage |

| Liability Coverage | ✓ | ✓ |

| Collision Coverage | ✗ | ✓ |

| Comprehensive Coverage | ✗ | ✓ |

| Theft Protection | ✗ | ✓ |

| Hail Damage | ✗ | ✓ |

| Fire Damage | ✗ | ✓ |

| Vehicle Repair Protection | Limited | Much Broader |

Real-World Example

Consider two drivers.

Both own vehicles worth approximately $22,000.

Both lose control during a winter storm and hit a guardrail.

Repair estimate:

$9,500

Driver A

Minimum coverage only.

Insurance payment:

$0

Out-of-pocket cost:

$9,500

Driver B

Full coverage.

Insurance payment:

$9,000

Deductible:

$500

Out-of-pocket cost:

$500

This example highlights the biggest distinction between the two options.

Minimum coverage protects others.

Full coverage helps protect your vehicle as well.

What This Means for Drivers

Choosing minimum coverage is often a financial trade-off.

You save money today through lower premiums.

However, you assume significantly more financial risk tomorrow.

Before reducing coverage, ask yourself:

“If my vehicle were seriously damaged next week, how would I pay for repairs or replacement?”

That question often provides more useful guidance than simply comparing monthly premiums.

Full Coverage vs Minimum Coverage Car Insurance

| Feature | Minimum Coverage | Full Coverage |

| Meets state legal requirements | Yes | Yes |

| Includes liability coverage | Yes | Yes |

| Covers damage to your own car after an accident | No | Yes, through collision coverage |

| Covers theft | No | Yes, through comprehensive coverage |

| Covers hail, fire, vandalism, and falling objects | No | Yes, through comprehensive coverage |

| Usually required by lenders or leasing companies | No | Yes |

| Monthly premium | Lower | Higher |

| Financial protection after vehicle damage | Limited | Broader |

Full Coverage vs Liability-Only Insurance

Many consumers use the terms “minimum coverage” and “liability-only insurance” interchangeably.

While they are closely related, understanding the distinction remains important.

Liability-Only Insurance Protects

- Other drivers

- Other vehicles

- Property you damage

Generally does not protect:

- Your vehicle

Full Coverage Insurance Protects

- Other drivers

- Other vehicles

- Your vehicle

- Certain non-collision risks

Who Usually Chooses Liability-Only Insurance?

Common examples include:

- Owners of older vehicles

- Drivers with limited budgets

- Individuals with substantial emergency savings

- People who could comfortably replace their vehicle themselves

However, choosing liability-only coverage increases your financial exposure if your vehicle is:

- Stolen

- Totaled

- Vandalized

- Damaged in an accident

Common Consumer Mistake

Many drivers focus exclusively on vehicle age.

A ten-year-old vehicle may still be worth protecting.

The better question is:

Could I comfortably replace this vehicle tomorrow if it disappeared today?

If the answer is no, maintaining full coverage may still be the financially safer decision.

Key Takeaway

The decision between liability-only insurance and full coverage should be based less on vehicle age and more on your financial situation.

If a major repair or replacement would create hardship, broader coverage may continue to provide meaningful value.

What Full Coverage Does Not Cover

One of the biggest misunderstandings in auto insurance is believing that full coverage means unlimited protection.

It doesn’t.

Even the most comprehensive auto insurance policy has exclusions. Knowing what your policy does not cover can be just as important as understanding what it does cover.

Many claim disputes happen because drivers assume a loss is covered without reviewing the policy details beforehand.

Understanding these limitations can help you make better insurance decisions and avoid unpleasant surprises during the claims process.

Maintenance and Normal Wear and Tear

Insurance is designed to cover sudden and accidental losses.

It is not a maintenance plan.

Most policies generally do not cover:

- Oil changes

- Brake replacement

- Tire wear

- Battery replacement

- Engine deterioration

- Transmission wear

These expenses are considered part of normal vehicle ownership.

Common Consumer Mistake

Many drivers assume that because they have full coverage, major repair bills should be covered automatically.

In reality, insurance and maintenance serve completely different purposes.

Mechanical Breakdowns

Suppose your vehicle’s transmission fails after 120,000 miles.

Repair estimate:

$6,500

Many vehicle owners assume insurance should help.

In most cases, it won’t.

Mechanical failures caused by age, wear, or maintenance issues are generally excluded.

However, if a mechanical problem results directly from a covered accident, coverage may apply.

This distinction catches many consumers off guard.

Personal Property Inside the Vehicle

Imagine your vehicle is broken into overnight.

A thief steals:

- A laptop

- A tablet

- Camera equipment

Your comprehensive coverage may help pay for damage to the vehicle.

However, the stolen items themselves are often covered under:

- Homeowners insurance

- Renters insurance

rather than auto insurance.

Intentional Damage

Insurance generally does not cover intentional acts.

Examples include:

- Deliberately damaging your vehicle

- Staged accidents

- Insurance fraud

Such claims are typically denied and may lead to legal consequences.

Racing and Illegal Activities

Most policies exclude losses occurring during:

- Street racing

- Organized racing events

- Criminal activity

Although coverage rules vary by insurer, these exclusions are extremely common.

What This Means for Drivers

A good rule of thumb is:

Insurance protects against unexpected accidents and covered events. It does not replace routine maintenance, warranties, or responsible vehicle ownership.

Understanding that difference can prevent costly misunderstandings later.

Full Coverage Insurance Deductibles Explained

Few insurance terms create more confusion than deductibles.

Yet deductibles have a major impact on:

- Premium costs

- Claim payouts

- Out-of-pocket expenses

Understanding how they work is essential when choosing coverage.

What Is a Deductible?

A deductible is the amount you agree to pay before insurance contributes toward a covered claim.

Common deductible amounts include:

- $250

- $500

- $1,000

- $2,000

The deductible typically applies to:

- Collision claims

- Comprehensive claims

It generally does not apply to liability claims.

Example

Suppose your vehicle suffers $6,000 in covered damage.

Deductible:

$500

Insurance payment:

$5,500

Your responsibility:

$500

The deductible represents your share of the loss.

Higher Deductible vs Lower Deductible

| Deductible | Monthly Premium | Out-of-Pocket Cost After Claim |

| $250 | Higher | Lower |

| $500 | Moderate | Moderate |

| $1,000 | Lower | Higher |

| $2,000 | Lowest | Highest |

Which Deductible Is Best?

There is no perfect answer.

A higher deductible may work well if you:

- Have strong emergency savings

- Rarely file claims

- Want lower monthly premiums

A lower deductible may make sense if you:

- Have limited savings

- Prefer predictable costs

- Want more financial protection after an accident

Financial Trade-Off Many Drivers Miss

Imagine:

Premium savings:

$12 per month

Annual savings:

$144

Deductible increase:

From $500 to $2,000

Additional out-of-pocket exposure:

$1,500

Many drivers focus only on the monthly savings.

They never ask:

“Could I comfortably pay a $2,000 deductible tomorrow if I had an accident?”

That question often leads to a much better decision.

How Much Does Full Coverage Car Insurance Cost?

One of the most common questions drivers ask is:

“How much does full coverage car insurance cost?”

The honest answer:

It depends.

There is no national price that applies to everyone.

Premiums can vary dramatically between drivers.

Factors That Affect Cost

Insurance companies evaluate many variables.

Driver Factors

- Age

- Driving experience

- Accident history

- Claims history

- Traffic violations

Vehicle Factors

- Vehicle value

- Repair costs

- Theft rates

- Safety features

Location Factors

- State

- ZIP code

- Local accident rates

- Weather risks

Policy Factors

- Deductibles

- Coverage limits

- Optional endorsements

Why New Vehicles Often Cost More to Insure

Modern vehicles contain:

- Cameras

- Sensors

- Radar systems

- Advanced safety technology

While these systems improve safety, they can also increase repair costs.

A minor accident involving a modern bumper may require thousands of dollars in repairs and sensor recalibration.

How to Find Affordable Full Coverage Insurance

Full coverage doesn’t always mean expensive coverage.

Several strategies can help reduce costs.

Shop Multiple Quotes

Comparing insurers remains one of the most effective ways to save money.

Raise Your Deductible Carefully

A modest increase may reduce premiums.

Just make sure the deductible remains affordable.

Bundle Policies

Many insurers offer discounts for combining:

- Auto insurance

- Homeowners insurance

- Renters insurance

Maintain a Clean Driving Record

Safe drivers often qualify for lower premiums.

Review Coverage Every Year

Your vehicle value, financial situation, and insurance needs change over time.

Annual reviews help ensure you’re not paying for coverage you no longer need.

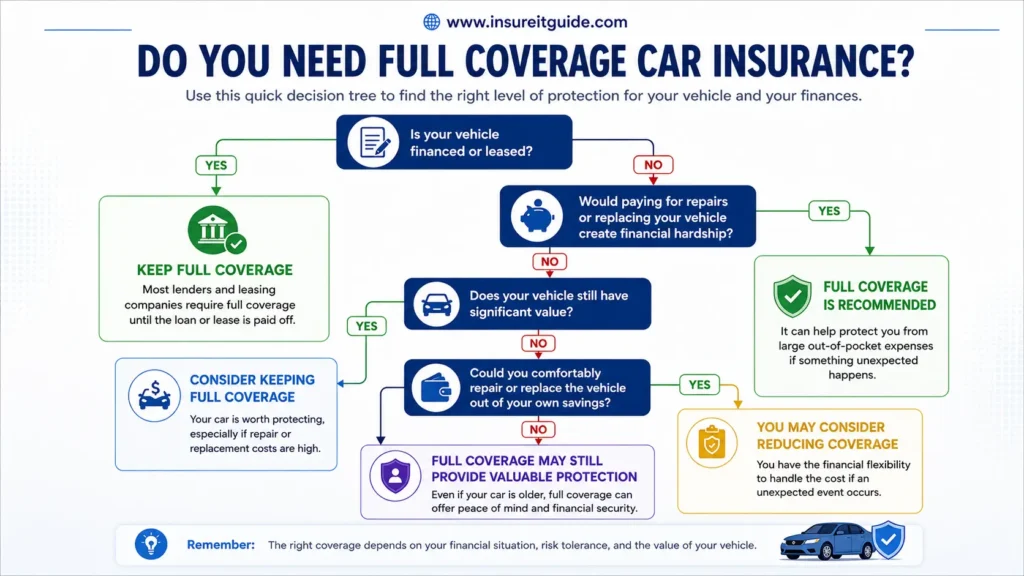

Is Full Coverage Car Insurance Worth It?

This is ultimately the question most drivers want answered.

The truth is:

There is no universal answer.

The right decision depends on:

- Vehicle value

- Financial situation

- Risk tolerance

- Emergency savings

Full Coverage Often Makes Sense When

Your Vehicle Has Significant Value

If your vehicle is worth:

- $15,000

- $20,000

- $30,000+

a major accident or theft could create substantial financial hardship.

Your Vehicle Is Financed

Most lenders require:

- Collision coverage

- Comprehensive coverage

until the loan is paid off.

Your Vehicle Is Leased

Leasing companies almost always require full coverage.

You Cannot Easily Replace the Vehicle

This is often the most important factor.

Ask yourself:

“If my vehicle disappeared tomorrow, could I comfortably replace it?”

If the answer is no, full coverage may still provide meaningful protection.

DECISION TREE HERE

When Should You Drop Full Coverage Insurance?

Many drivers search for a simple rule.

Unfortunately, none exists.

There is no specific age or mileage where dropping coverage automatically makes sense.

Consider Reviewing Coverage When

- Vehicle value has declined substantially

- Premiums continue increasing

- Emergency savings have grown

Common Consumer Mistake

Many drivers focus entirely on vehicle age.

In reality:

Vehicle age matters far less than replacement cost and personal finances.

A ten-year-old vehicle may still be expensive to replace.

Practical Rule of Thumb

Many insurance professionals suggest reviewing collision and comprehensive coverage when:

Annual premium plus deductible approaches 10% to 15% of the vehicle’s value.

This is not a strict rule, but it can be a useful starting point.

Common Myths About Full Coverage Insurance

Insurance myths often lead to poor decisions.

Myth #1

Full Coverage Covers Everything

Reality:

Every policy contains exclusions and limitations.

Myth #2

Full Coverage Means Unlimited Coverage

Reality:

Policies contain limits, deductibles, and conditions.

Myth #3

Older Cars Never Need Full Coverage

Reality:

Replacement cost and financial circumstances matter more than age alone.

Myth #4

Full Coverage Prevents Premium Increases

Reality:

Claims may still affect future premiums.

Myth #5

Comprehensive Coverage Only Covers Theft

Reality:

Comprehensive coverage may also help cover:

- Hail

- Flooding

- Vandalism

- Falling objects

- Animal collisions

Frequently Asked Questions

What is included in full coverage car insurance?

Short answer:

Liability, collision, and comprehensive coverage.

Depending on the insurer, drivers may also add optional protections such as roadside assistance, rental reimbursement, or uninsured motorist coverage.

Does full coverage insurance cover theft and accidents?

Yes.

Theft is generally covered under comprehensive coverage, while accident damage to your vehicle is generally covered under collision coverage.

Is full coverage car insurance required by law?

No.

Most states only require liability insurance. However, lenders and leasing companies often require full coverage.

Does full coverage cover engine failure?

Usually not.

Mechanical failures caused by wear and tear are generally excluded.

Does full coverage cover rental cars?

Not automatically.

Rental reimbursement coverage is usually an optional add-on.

What is the difference between liability and full coverage insurance?

Liability protects others.

Full coverage helps protect both other people and your own vehicle.

Key Takeaways

- Full coverage is not an official insurance policy.

- It generally includes liability, collision, and comprehensive coverage.

- Collision coverage protects your vehicle after accidents.

- Comprehensive coverage protects against theft, hail, vandalism, and other non-collision losses.

- Deductibles affect both premiums and claim payouts.

- Full coverage is often valuable for financed, leased, newer, or higher-value vehicles.

- Coverage decisions should be based on financial risk rather than vehicle age alone.

Conclusion

Full coverage car insurance remains one of the most valuable forms of financial protection available to drivers, but it is also one of the most misunderstood.

Despite the name, full coverage does not cover every possible loss. Instead, it typically combines liability, collision, and comprehensive coverage to provide broader protection against many of the risks vehicle owners face every day.

For some drivers, maintaining full coverage can prevent a serious financial setback after an accident, theft, hailstorm, or total loss. For others, especially those with lower-value vehicles and substantial savings, reducing coverage may eventually make sense.

The key is not asking:

“How old is my vehicle?”

Instead ask:

“Would replacing this vehicle tomorrow create financial hardship?”

If the answer is yes, maintaining full coverage may still be a wise decision.

Ultimately, the best insurance decision balances affordability with financial protection. Understanding what your policy covers, what it excludes, and how much risk you’re willing to accept will help you make a more informed choice.

At InsureItGuide.com, our goal is to help drivers understand insurance with confidence so they can make smarter decisions that protect both their vehicles and their finances.