Buying auto insurance should feel simple.

You pay a monthly premium, receive proof of insurance, and assume you are financially protected if something goes wrong.

But for many drivers, the real confusion begins when they actually open the insurance policy.

Suddenly they see terms like

- Liability limits

- Collision coverage

- Comprehensive insurance

- Deductibles

- Exclusions

- Actual cash value

- Uninsured motorist coverage

- Declarations page

For beginner drivers and first-time insurance buyers, these terms can feel overwhelming.

Unfortunately, many people purchase auto insurance without fully understanding what their policy actually covers.

That becomes a serious problem after accidents.

Drivers often discover too late that

- their deductible is much higher than expected

- their policy excludes certain damage

- their liability limits are too low

- full coverage does not literally mean “everything.”

- their insurer only pays actual cash value after total losses

These misunderstandings happen every day across the United States.

And they can become extremely expensive.

Modern vehicles cost far more to repair than older vehicles because they contain the following:

- cameras

- radar systems

- sensors

- advanced electronics

- lane-assist systems

- adaptive cruise control technology

Even relatively small accidents can generate repair bills worth thousands of dollars.

That is why understanding your auto insurance policy matters so much.

If you have ever asked:

- How do I read and understand my auto insurance policy?

- What does each part of a car insurance policy mean?

- What is included in a standard auto insurance policy?

- How does auto insurance coverage work after an accident?

- What should beginner drivers know about car insurance policies?

This complete guide will help you understand everything clearly.

In this detailed article, you will learn:

- how auto insurance policies work

- what the declarations page means

- how liability insurance works

- what collision and comprehensive coverage actually protect

- how deductibles affect claims

- common policy exclusions

- how claims work after accidents

- how to avoid expensive insurance mistakes

- how to choose better protection

By the end of this guide, you will understand your insurance policy far more confidently and make smarter financial decisions as a driver.

────────────────────────────────────────

Table of Contents

- What Is an Auto Insurance Policy?

- Why Auto Insurance Matters

- Understanding the Auto Insurance Declarations Page

- Liability Insurance Explained

- Collision Coverage Explained

- Comprehensive Coverage Explained

- Understanding Insurance Deductibles

- Uninsured and Underinsured Motorist Coverage

- Medical Payments and Personal Injury Protection

- Full Coverage Insurance Explained

- Common Auto Insurance Terms Explained

- What Auto Insurance Usually Does NOT Cover

- How Claims Work After an Accident

- How Insurance Companies Determine Premiums

- Common Auto Insurance Mistakes Drivers Make

- How to Save Money on Auto Insurance

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

────────────────────────────────────────

What Is an Auto Insurance Policy?

An auto insurance policy is a legal contract between you and an insurance company.

In exchange for paying premiums, the insurer agrees to provide financial protection for covered losses.

Auto insurance policies help drivers manage financial risks associated with:

- vehicle accidents

- injuries

- lawsuits

- property damage

- theft

- weather damage

- medical expenses

Without insurance, even a moderate accident could create devastating financial consequences, for example:

- vehicle repairs

- emergency room bills

- legal claims

- lost wages

- rehabilitation costs

can quickly reach tens of thousands of dollars.

Insurance exists to reduce that financial risk.

Every policy contains detailed information about:

- coverage types

- policy limits

- exclusions

- deductibles

- insured drivers

- covered vehicles

- claim procedures

Many drivers never read their policy documents carefully. Instead, they focus mainly on the following:

- monthly premium cost

- payment schedule

- insurance ID cards

Understanding the actual policy details is extremely important because insurance policies determine:

- what is covered

- what is not covered

- how much protection exists

- how claims are handled

The difference between a strong policy and a weak policy can become financially life-changing after major accidents.

────────────────────────────────────────

────────────────────────────────────────

Why Auto Insurance Matters

Auto insurance is not just about following state laws.

It is about financial protection.

Car accidents happen every day across the United States.

Even careful drivers face risks from:

- distracted drivers

- severe weather

- uninsured drivers

- heavy traffic

- road hazards

- theft

- vandalism

Modern vehicles are also becoming increasingly expensive to repair.

Today’s cars contain:

- advanced safety systems

- cameras

- sensors

- complex electronics

Even relatively minor damage may require the following:

- expensive replacement parts

- recalibration procedures

- specialized labor

Medical costs are even more expensive.

A short emergency room visit combined with imaging scans and ambulance transportation can cost thousands of dollars.

Without insurance, drivers may face the following:

- lawsuits

- wage garnishment

- debt

- financial hardship

- vehicle replacement costs

That is why nearly every state requires drivers to maintain at least minimum liability insurance.

However, state minimum coverage is not always enough to fully protect drivers financially.

Understanding your policy helps you:

- reduce financial risk

- avoid coverage gaps

- make smarter insurance decisions

- protect long-term financial stability

Insurance is not simply a legal requirement.

It is a major financial safety tool.

────────────────────────────────────────

────────────────────────────────────────

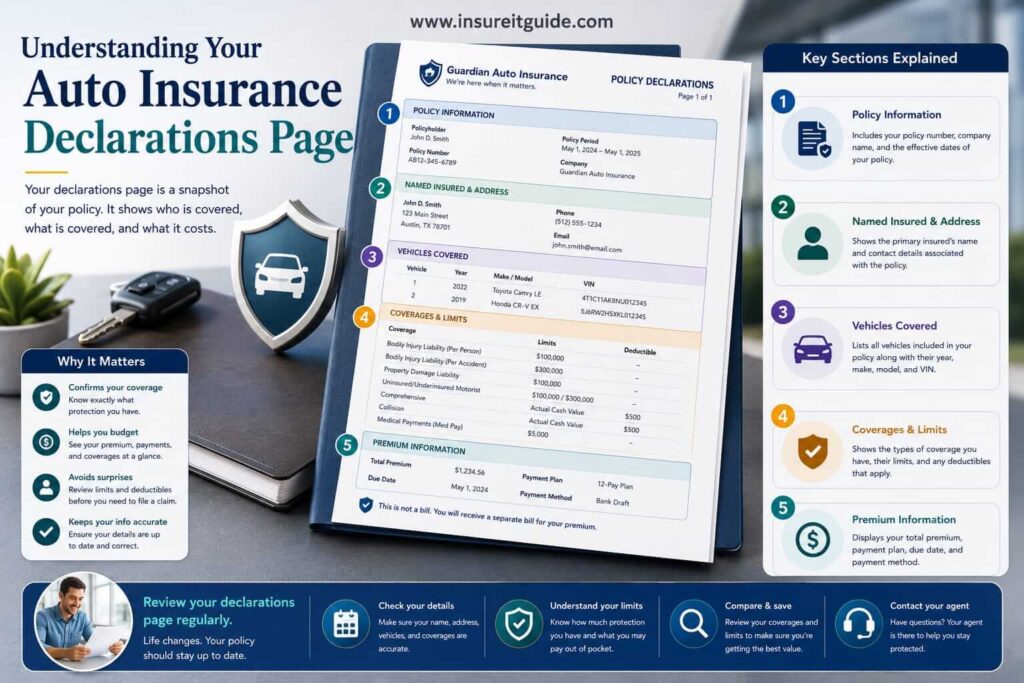

Understanding the Auto Insurance Declarations Page

One of the most important sections of your policy is the declarations page.

This section acts like the summary page for your insurance coverage.

The declarations page usually contains the following:

- policy number

- insured drivers

- covered vehicles

- policy dates

- premiums

- deductibles

- coverage limits

Think of it as the “quick overview” of your insurance policy.

Most insurers place this section near the beginning of the policy document.

Drivers should review the declarations page carefully because it confirms the following:

- what coverage exists

- how much protection you purchased

- how much your deductibles are

- whether policy details are correct

For example, liability coverage may appear like this:

100/300/100

This usually means:

- $100,000 bodily injury liability per person

- $300,000 bodily injury liability per accident

- $100,000 property damage liability

Many drivers misunderstand these numbers.

That confusion can become dangerous after serious accidents involving:

- injuries

- multiple vehicles

- lawsuits

Drivers should review declaration pages whenever:

- buying new vehicles

- moving states

- adding drivers

- renewing policies

- making coverage changes

Mistakes on the declarations page can create major claim problems later.

────────────────────────────────────────

────────────────────────────────────────

Liability Insurance Explained

Liability insurance is the foundation of most auto insurance policies.

In most U.S. states, liability insurance is legally required before drivers can operate vehicles on public roads.

Liability insurance protects other people when you cause accidents.

This is one of the most misunderstood parts of auto insurance.

Many drivers mistakenly believe liability insurance repairs their own vehicle.

Usually, it does not.

Liability insurance mainly protects you from financial responsibility toward others.

There are usually two major parts:

Bodily Injury Liability

This helps pay for:

- medical expenses

- hospital bills

- rehabilitation costs

- lost wages

- legal claims

Property Damage Liability

This helps pay for:

- vehicle repairs

- fence damage

- building repairs

- public property damage

Medical costs in the United States are extremely expensive.

Even moderate accidents can create the following:

- ambulance expenses

- emergency treatment costs

- surgery bills

- long-term rehabilitation expenses

Property damage claims are also increasing because modern vehicles contain expensive electronics and safety systems.

This is why many financial professionals recommend liability limits above state minimum requirements.

Low liability limits may expose drivers to:

- lawsuits

- wage garnishment

- asset seizure

Choosing stronger liability coverage often provides better financial protection.

────────────────────────────────────────

────────────────────────────────────────

Collision Coverage Explained

Collision coverage helps repair or replace your vehicle after accidents involving collisions.

Unlike liability insurance, collision coverage protects your own vehicle.

Collision insurance may apply after the following:

- hitting another vehicle

- striking a pole

- crashing into a guardrail

- single-car accidents

- rollovers

For example, suppose you slide on a wet road and crash into a barrier.

Your vehicle suffers severe front-end damage.

Collision coverage may help pay for repairs.

Modern vehicles are increasingly expensive to repair because they contain the following:

- sensors

- radar systems

- cameras

- advanced electronics

Even damaged bumpers may require:

- recalibration

- diagnostics

- specialized repairs

Collision coverage becomes especially valuable for:

- newer vehicles

- financed vehicles

- leased vehicles

- high-value cars

Without collision coverage, drivers may need to pay repair costs entirely out of pocket.

Many lenders require collision insurance for financed vehicles because the lender still holds financial interest in the car.

────────────────────────────────────────

────────────────────────────────────────

Comprehensive Coverage Explained

Comprehensive insurance protects against non-collision vehicle damage.

This coverage usually applies to events outside the driver’s direct control.

Examples include:

- theft

- fire

- flooding

- hail damage

- vandalism

- falling objects

- storm damage

- animal collisions

Suppose a hailstorm damages your parked vehicle overnight.

Because the damage was not caused by a driving collision, comprehensive insurance may apply instead of collision coverage.

Comprehensive insurance is especially valuable in areas prone to:

- hurricanes

- flooding

- wildfires

- severe storms

- vehicle theft

Many drivers underestimate how common non-collision vehicle damage actually is.

Weather-related claims continue increasing across the United States every year.

Animal collisions are another important example.

Many drivers are surprised to learn hitting a deer usually falls under comprehensive coverage rather than collision coverage.

Without comprehensive insurance, drivers may face major out-of-pocket expenses after unpredictable events.

────────────────────────────────────────

────────────────────────────────────────

Understanding Insurance Deductibles

A deductible is the amount you pay out of pocket before insurance coverage begins paying covered claim costs.

For example:

- repair cost: $5,000

- deductible: $500

- insurance company pays: $4,500

Deductibles commonly apply to:

- collision coverage

- comprehensive coverage

Higher deductibles usually lower monthly premiums.

Lower deductibles usually increase premiums.

Choosing the right deductible depends on:

- emergency savings

- financial stability

- vehicle value

- risk tolerance

Many drivers focus only on reducing premiums and accidentally choose deductibles they cannot realistically afford later.

That can create financial stress after accidents.

Some drivers choose:

- higher collision deductibles

- lower comprehensive deductibles

because weather-related or glass claims may happen more frequently.

Choosing the right deductible is about balancing:

- affordability

- financial protection

- long-term risk management

────────────────────────────────────────

────────────────────────────────────────

Uninsured and Underinsured Motorist Coverage

Millions of drivers across the United States remain uninsured or underinsured.

That creates major financial risk after accidents.

Uninsured motorist coverage helps protect you if an uninsured driver causes an accident.

Underinsured motorist coverage helps when the at-fault driver’s insurance limits are too low.

These coverages may help pay for:

- medical expenses

- lost wages

- vehicle damage in some states

Imagine a driver causes a serious accident but only carries minimal liability insurance.

Medical bills exceed their policy limits.

Without uninsured or underinsured motorist protection, you may face significant financial losses.

These coverages become especially important in states with high uninsured driver rates.

Many financial professionals consider uninsured motorist protection one of the most valuable optional coverages.

────────────────────────────────────────

────────────────────────────────────────

Medical Payments and Personal Injury Protection

Some policies include:

- Medical Payments coverage (MedPay)

- Personal Injury Protection (PIP)

These coverages help pay medical expenses after accidents regardless of fault.

Coverage may include:

- ambulance transportation

- emergency room bills

- hospital expenses

- rehabilitation costs

PIP coverage may also help pay:

- lost wages

- essential service costs

Some states require PIP coverage because they operate under no-fault insurance systems.

No-fault systems reduce lawsuits by requiring drivers to use their own insurance first for certain medical expenses.

Understanding whether your state uses no-fault insurance is important because rules vary considerably across the country.

────────────────────────────────────────

────────────────────────────────────────

Full Coverage Insurance Explained

Many drivers use the phrase “full coverage insurance.”

However, full coverage is not an official insurance product.

Usually, full coverage refers to:

- liability insurance

- collision coverage

- comprehensive coverage

Some drivers mistakenly assume full coverage means literally every type of damage is covered.

That is not true.

Policies still contain:

- exclusions

- deductibles

- limitations

For example, full coverage usually does not pay for:

- mechanical breakdowns

- normal wear and tear

- aftermarket custom equipment unless added

Understanding these limitations is extremely important.

Financed and leased vehicles often require full coverage because lenders want protection for the vehicle itself.

Full coverage generally costs more than liability-only insurance, but it also provides broader financial protection.

────────────────────────────────────────

────────────────────────────────────────

Common Auto Insurance Terms Explained

Insurance policies contain many confusing terms.

Understanding these definitions helps drivers read policies more confidently.

Premium

The amount you pay for insurance coverage.

Deductible

The amount you pay before insurance begins covering claim costs.

Policy Limit

The maximum amount an insurer may pay for covered losses.

Exclusion

Situations not covered by the policy.

Actual Cash Value

The depreciated value of your vehicle.

Total Loss

When repair costs exceed vehicle value.

Endorsement

An addition or modification to your policy.

Claim

A request for insurance payment after a covered loss.

Understanding these terms helps drivers avoid confusion during claims.

────────────────────────────────────────

────────────────────────────────────────

What Auto Insurance Usually Does NOT Cover

Many drivers assume insurance covers everything.

In reality, policies contain exclusions.

Common exclusions may include:

- mechanical failures

- normal wear and tear

- intentional damage

- racing activities

- commercial use without proper coverage

For example:

- engine breakdowns

- worn tires

- maintenance problems

usually are not covered.

Understanding exclusions is just as important as understanding coverage.

Drivers should carefully review policy limitations before accidents happen.

────────────────────────────────────────

────────────────────────────────────────

How Claims Work After an Accident

Understanding the claims process helps drivers feel less overwhelmed after accidents.

The process usually includes:

1. Reporting the accident

2. Filing the claim

3. Damage inspection

4. Coverage review

5. Repair estimates

6. Claim settlement

Drivers should:

- take photos

- exchange information

- contact police when necessary

- notify insurers quickly

Claims may involve:

- liability investigations

- fault determinations

- repair estimates

- deductible payments

Understanding your policy before accidents happen can make the claims process much smoother.

────────────────────────────────────────

────────────────────────────────────────

How Insurance Companies Determine Premiums

Insurance premiums are based on risk.

Factors may include:

- driving history

- age

- location

- vehicle type

- claim history

- credit-based insurance scores in some states

High-risk drivers generally pay more because insurers predict higher claim likelihood.

Vehicles with expensive repair costs may also increase premiums.

Drivers can often reduce costs by:

- maintaining clean driving records

- comparing quotes

- bundling policies

- improving credit in eligible states

Understanding these factors helps drivers make smarter insurance decisions.

────────────────────────────────────────

────────────────────────────────────────

Common Auto Insurance Mistakes Drivers Make

Many drivers accidentally make expensive insurance mistakes.

Common examples include:

- choosing minimum coverage only because it is cheaper

- ignoring deductibles

- misunderstanding full coverage

- failing to review policies annually

- underestimating liability risks

Insurance decisions should focus on long-term financial protection, not just monthly premiums.

Reviewing coverage regularly helps drivers avoid dangerous coverage gaps.

────────────────────────────────────────

────────────────────────────────────────

How to Save Money on Auto Insurance

Drivers can often reduce insurance costs without sacrificing important protection.

Strategies include:

- comparing quotes regularly

- maintaining clean driving records

- bundling policies

- asking about discounts

- improving credit in eligible states

- choosing appropriate deductibles

Insurance pricing varies dramatically between companies.

Comparison shopping remains one of the most effective ways to reduce costs.

────────────────────────────────────────

────────────────────────────────────────

Frequently Asked Questions

How do I read and understand my auto insurance policy?

Start with the declarations page, then review coverage types, deductibles, limits, and exclusions carefully.

What does each part of a car insurance policy mean?

Each section explains different protections, including liability, collision, comprehensive coverage, deductibles, and policy conditions.

What is included in a standard auto insurance policy?

Most policies include liability coverage and optional protections such as collision and comprehensive insurance.

How does auto insurance coverage work after an accident?

Coverage depends on fault, policy details, deductibles, and claim circumstances.

What should beginner drivers know about car insurance policies?

Drivers should understand deductibles, liability limits, exclusions, and how claims work before purchasing coverage.

────────────────────────────────────────

Key Takeaways

- Auto insurance policies are legal contracts providing financial protection.

- Liability insurance protects other people after accidents.

- Collision coverage protects your own vehicle after crashes.

- Comprehensive coverage protects against non-collision damage.

- Deductibles affect both premiums and claim costs.

- Understanding policy terms helps drivers avoid expensive mistakes.

- Reviewing coverage regularly improves financial protection.

────────────────────────────────────────

Final Thoughts

Understanding your auto insurance policy is one of the most important parts of becoming a financially responsible driver.

Insurance policies may initially feel confusing, but learning the meaning of common coverage types and insurance terms can help drivers make smarter financial decisions and avoid costly surprises later.

The best insurance policy is not always the cheapest one.

The goal should always be balancing affordability with meaningful financial protection.

Drivers should review their auto insurance policy regularly, ask questions whenever something is unclear, and ensure their coverage aligns with their financial needs, driving habits, and potential risk exposure.

For more beginner-friendly insurance guides, educational financial content, and practical coverage comparisons, visit www.insureitguide.com