Buying car insurance can feel surprisingly confusing.

Most drivers understand basic ideas like monthly premiums and insurance cards. But once terms like “deductible,” “collision coverage,” “comprehensive claims,” and “policy limits” appear, many people start feeling overwhelmed.

And yet, understanding deductibles is extremely important.

Your deductible directly affects:

- Your monthly insurance premium

- Your out-of-pocket costs after accidents

- Your financial risk

- Your claims experience

- The overall affordability of your insurance policy

Unfortunately, many drivers choose deductibles without fully understanding how they actually work.

Some people select extremely high deductibles to reduce monthly payments, only to realize later they cannot comfortably afford the deductible after an accident.

Others choose low deductibles without realizing how much more they may pay in premiums over time.

That is why understanding insurance deductibles matters so much.

If you have ever asked:

- What is an insurance deductible?

- How does an insurance deductible work?

- Do you pay a deductible if the accident was not your fault?

- Is a higher deductible better for car insurance?

- What happens if repair costs are lower than the deductible?

This complete guide will help you understand everything clearly.

In this article, you will learn:

- What insurance deductibles actually are

- How deductibles work after accidents

- The difference between deductibles and premiums

- How collision and comprehensive deductibles work

- How deductibles affect insurance costs

- How to choose the right deductible

- Common deductible mistakes drivers make

- Real-world deductible examples

- Smart ways to save money on insurance

By the end of this guide, you will understand exactly how insurance deductibles work and how to choose a deductible that fits your financial situation.

Table of Contents

- What Is an Insurance Deductible?

- Why Insurance Deductibles Exist

- How Insurance Deductibles Work

- Deductible vs. Premium: What’s the Difference?

- Collision Deductible Explained

- Comprehensive Insurance Deductible Explained

- When Do You Pay a Deductible?

- Do You Pay a Deductible If the Accident Was Not Your Fault?

- What Happens If Damage Costs Less Than the Deductible?

- High vs Low Deductible Insurance

- How Deductibles Affect Insurance Premiums

- How to Choose the Right Deductible

- Common Insurance Deductible Mistakes

- Ways to Save Money Without Choosing a Risky Deductible

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

What Is an Insurance Deductible?

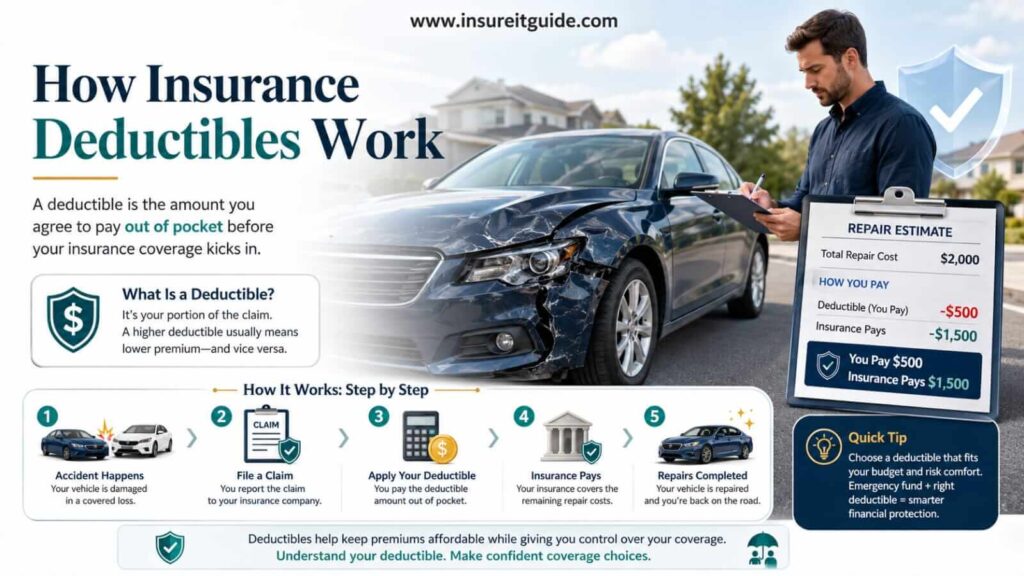

An insurance deductible is the amount of money you agree to pay out of pocket before your insurance company helps pay the remaining covered claim costs.

In simple terms, the deductible represents your share of financial responsibility during a claim.

For example:

- Repair bill: $4,000

- Deductible: $500

- Insurance company pays: $3,500

You pay the first $500.

The insurer covers the remaining eligible amount.

Deductibles are most commonly associated with:

- Collision coverage

- Comprehensive coverage

- Health insurance

- Homeowners insurance

In auto insurance, deductibles mainly apply to damage involving your own vehicle.

Liability insurance generally does not include a deductible because liability coverage protects other people after accidents you cause.

Insurance deductibles exist because they help reduce:

- Small claims

- Insurance fraud

- Excessive claim frequency

- Overall insurance costs

By requiring policyholders to share some financial responsibility, insurers can keep premiums more manageable.

This balance between deductibles and premiums is one of the most important parts of insurance pricing.

Why Insurance Deductibles Exist

Many drivers wonder why deductibles exist at all.

Why doesn’t insurance simply pay the full amount immediately?

The answer involves risk sharing.

Insurance companies are designed to protect drivers against significant financial losses, not necessarily every small expense.

Without deductibles, insurers would receive enormous numbers of very small claims.

For example:

- Minor scratches

- Small dents

- Tiny windshield chips

- Cosmetic damage

Processing huge volumes of small claims would dramatically increase insurance costs for everyone.

Deductibles help create a balance.

They encourage drivers to:

- Avoid unnecessary claims

- Share some financial responsibility

- Use insurance primarily for meaningful losses

This system helps stabilize insurance pricing.

Deductibles also reduce insurance fraud.

Without deductibles, fraudulent claims could become more common because policyholders would face little financial consequence for filing minor or questionable claims.

Another reason deductibles exist is risk management.

Drivers who choose higher deductibles are effectively agreeing to accept more personal financial risk in exchange for lower monthly premiums.

Drivers who choose lower deductibles shift more financial risk to the insurance company but usually pay higher premiums.

This flexibility allows policyholders to customize insurance based on:

- Budget

- Emergency savings

- Risk tolerance

- Vehicle value

- Driving habits

Understanding this tradeoff is essential when choosing coverage.

How Insurance Deductibles Work

Insurance deductibles are relatively straightforward once you see real-world examples.

Let’s look at several practical scenarios.

Example 1: Collision Claim

Suppose you accidentally rear-end another vehicle.

Your car suffers $6,000 in repair damage.

Your collision deductible is $1,000.

In this case:

- You pay: $1,000

- Insurance company pays: $5,000

Example 2: Comprehensive Claim

A severe hailstorm damages your parked vehicle.

Repair costs total $3,500.

Your comprehensive deductible is $500.

In this situation:

- You pay: $500

- Insurance company pays: $3,000

Example 3: Small Claim Below Deductible

Your bumper repair costs only $400.

Your deductible is $1,000.

Because repair costs are below the deductible:

- You pay the full $400

- The insurance company pays nothing

This is why drivers should think carefully before filing small claims.

In some situations, paying minor repair costs yourself may make more financial sense than filing claims.

Frequent claims can sometimes affect future insurance pricing.

Understanding how deductibles work helps drivers make smarter claim decisions.

Deductible vs. Premium: What’s the Difference?

One of the most common insurance misunderstandings involves confusing deductibles with premiums.

These are completely different concepts.

Insurance Premium

Your premium is the amount you pay regularly to maintain insurance coverage.

This may be:

- Monthly

- Quarterly

- Semi-annually

- Annually

Premiums are essentially the ongoing cost of your insurance policy.

Insurance Deductible

Your deductible is the amount you pay out of pocket before insurance coverage begins during a covered claim.

The relationship between deductibles and premiums is extremely important.

Higher Deductible = Lower Premium

Drivers willing to accept more financial risk usually receive lower monthly premiums.

Lower Deductible = Higher Premium

Drivers wanting less out-of-pocket risk generally pay higher premiums.

For example:

| Deductible | Monthly Premium |

| $250 | Higher |

| $500 | Moderate |

| $1,000 | Lower |

Choosing the right balance depends heavily on:

- Emergency savings

- Budget stability

- Financial comfort level

- Claim likelihood

Some drivers focus too heavily on lowering monthly premiums without considering whether they could realistically afford the deductible after a serious accident.

That can become financially stressful later.

Collision Deductible Explained

A collision deductible applies when your own vehicle is damaged in a collision-related accident.

Collision coverage generally helps pay for damage involving:

- Another vehicle

- Guardrails

- Poles

- Fences

- Single-car accidents

- Rollovers

For example, imagine sliding on a wet road and crashing into a guardrail.

Repair costs total $8,000.

If your collision deductible is $1,000:

- You pay: $1,000

- Insurance company pays: $7,000

Collision deductibles can vary significantly.

Common options include:

- $250

- $500

- $1,000

- $1,500

- $2,000

Drivers with newer vehicles often prefer lower collision deductibles because repair costs can become extremely expensive.

Modern vehicles contain:

- Cameras

- Sensors

- Advanced safety systems

- Expensive electronics

- Specialized calibration technology

Even relatively small accidents may generate large repair bills.

Choosing the right collision deductible depends heavily on:

- Vehicle value

- Financial situation

- Emergency savings

- Daily driving exposure

Comprehensive Insurance Deductible Explained

A comprehensive deductible applies when your vehicle suffers non-collision damage.

Comprehensive insurance may cover:

- Theft

- Hail damage

- Flood damage

- Fire

- Vandalism

- Falling objects

- Animal collisions

- Storm damage

For example, suppose a tree branch falls onto your parked vehicle during a storm.

Repair costs total $2,500.

Your comprehensive deductible is $500.

In this situation:

- You pay: $500

- Insurance company pays: $2,000

Many drivers choose lower comprehensive deductibles than collision deductibles.

Why?

Because comprehensive claims such as

- Windshield damage

- Hail damage

- Weather-related incidents

may occur more frequently.

Some insurers even offer special glass coverage with very low or zero deductibles.

Comprehensive insurance is especially valuable in areas prone to:

- Hurricanes

- Flooding

- Wildfires

- Hailstorms

- Vehicle theft

As severe weather events continue increasing across the United States, comprehensive coverage has become increasingly important.

When Do You Pay a Deductible?

Drivers often wonder exactly when deductibles apply.

In general, deductibles apply when:

- You file a claim involving your own vehicle

- The claim is covered

- Repair costs exceed the deductible amount

Deductibles commonly apply during:

- Collision claims

- Comprehensive claims

However, deductibles usually do NOT apply to liability insurance claims because liability insurance protects other people.

Here are common situations where deductibles may apply:

| Situation | Deductible Usually Applies? |

| Collision accident | Yes |

| Hail damage | Yes |

| Vehicle theft | Yes |

| Windshield damage | Usually |

| Liability claim against you | No |

Some drivers mistakenly believe they pay deductibles directly to insurance companies.

In many cases, the deductible is simply subtracted from the claim payout.

For example:

- Repair cost: $5,000

- Deductible: $500

- Insurance payment: $4,500

Understanding when deductibles apply helps drivers avoid surprises during claims.

Do You Pay a Deductible If the Accident Was Not Your Fault?

This is one of the most searched insurance questions online.

The answer depends on how the claim is handled.

In many situations, if another driver is clearly at fault and their insurer accepts responsibility, you may not ultimately pay a deductible.

However, the process can vary.

For example:

Scenario 1: Other Driver’s Insurance Pays Directly

If the at-fault driver’s insurance accepts liability quickly:

- Their insurer may pay repair costs directly

- You may avoid paying your deductible entirely

Scenario 2: Your Insurance Handles the Claim First

Sometimes your insurer may process repairs faster using your own collision coverage.

In that case:

- You may initially pay your deductible

- Your insurer later seeks reimbursement from the at-fault insurer

- You may eventually recover the deductible

This recovery process is called subrogation.

However, deductible reimbursement timelines vary.

In some situations:

- Liability disputes occur

- Fault percentages are shared

- Claims take longer to resolve

That is why some drivers temporarily pay deductibles even when they were not at fault.

Understanding this process helps reduce confusion after accidents.

What Happens If Damage Costs Less Than the Deductible?

If repair costs are lower than your deductible, insurance generally does not pay anything.

For example:

- Repair cost: $400

- Deductible: $1,000

Because the repair cost does not exceed the deductible:

- You pay the full amount

- No insurance payout occurs

This is why many drivers avoid filing very small claims.

Filing small claims may not provide financial benefit and could potentially influence future premiums depending on the insurer and claim history.

Drivers should carefully evaluate:

- Repair cost

- Deductible amount

- Potential future premium impact

before filing small claims.

Sometimes paying small repairs out of pocket makes more financial sense.

However, larger damage usually justifies using insurance coverage.

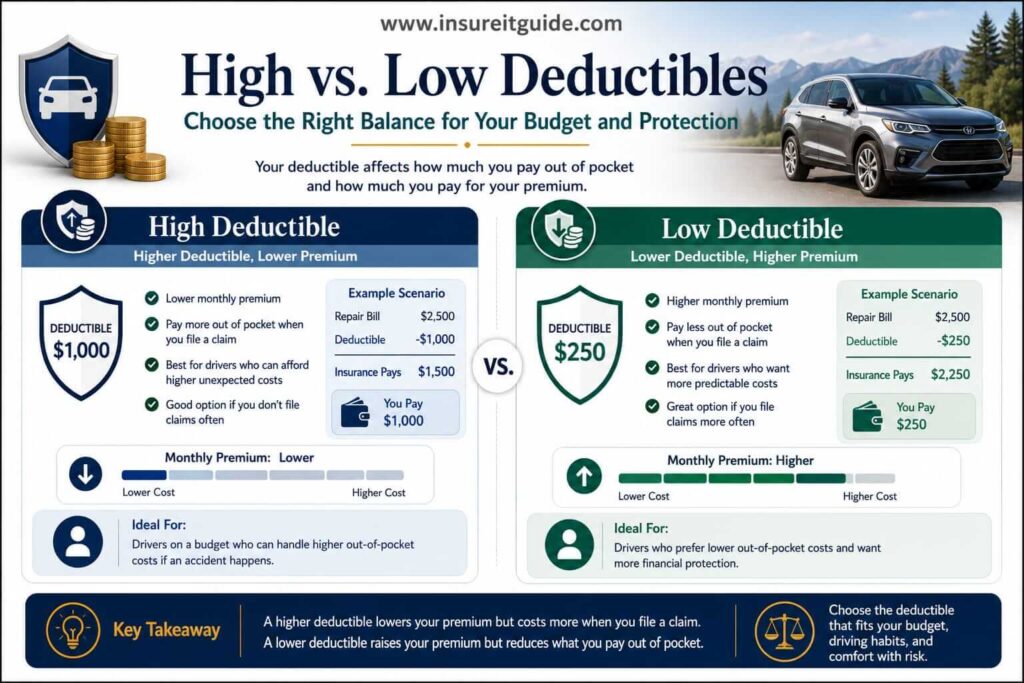

High vs Low Deductible Insurance

Choosing between high and low deductibles is one of the most important insurance decisions drivers make.

Both options have advantages and disadvantages.

High Deductible Insurance

Higher deductibles usually provide:

- Lower monthly premiums

- Reduced long-term insurance costs

However, they also create:

- Higher out-of-pocket expenses after claims

- Greater financial risk

High deductibles may make sense for drivers who:

- Have strong emergency savings

- Drive less frequently

- Want lower monthly bills

- Can comfortably absorb unexpected expenses

Low Deductible Insurance

Lower deductibles usually provide:

- Lower out-of-pocket costs after accidents

- Greater financial predictability

However, they also typically involve:

- Higher monthly premiums

Low deductibles may make sense for drivers who:

- Prefer financial stability

- Have limited emergency savings

- Drive frequently

- Own newer vehicles

The best deductible depends on balancing:

- Monthly affordability

- Financial risk tolerance

- Emergency savings

- Claim likelihood

There is no universal “perfect” deductible.

The right choice depends on your personal financial situation.

How Deductibles Affect Insurance Premiums

Insurance companies calculate premiums using risk.

Drivers choosing lower deductibles shift more financial risk to the insurer.

As a result, insurers usually charge higher premiums.

Drivers choosing higher deductibles accept more financial responsibility themselves.

That generally lowers insurance costs.

For example:

| Deductible | Approximate Premium Impact |

| $250 | Highest premium |

| $500 | Moderate premium |

| $1,000 | Lower premium |

However, cheaper premiums do not always mean better financial decisions.

Drivers choosing very high deductibles sometimes struggle financially after accidents.

For example:

- An accident occurs unexpectedly

- Repairs begin immediately

- Driver cannot comfortably afford deductible

This situation can create major financial stress.

Insurance decisions should balance:

- Monthly affordability

- Emergency savings

- Long-term risk management

The cheapest monthly premium is not always the smartest financial strategy.

How to Choose the Right Deductible

Choosing the right deductible depends on several important factors.

Emergency Savings

Could you comfortably afford the deductible tomorrow if an accident happened?

If not, the deductible may be too high.

Vehicle Value

Older vehicles may not justify extremely low deductibles.

Newer vehicles with expensive repair costs may benefit from stronger protection.

Driving Frequency

Drivers with long daily commutes face higher accident exposure.

Local Risks

Drivers living in areas prone to

- Hailstorms

- Flooding

- Theft

- Heavy traffic

may benefit from lower deductibles.

Financial Comfort Level

Some drivers prefer lower monthly costs.

Others prefer lower claim expenses.

Choosing the right deductible is ultimately about balancing:

- Monthly budget

- Risk tolerance

- Financial security

Insurance should support long-term financial stability rather than create unnecessary financial stress.

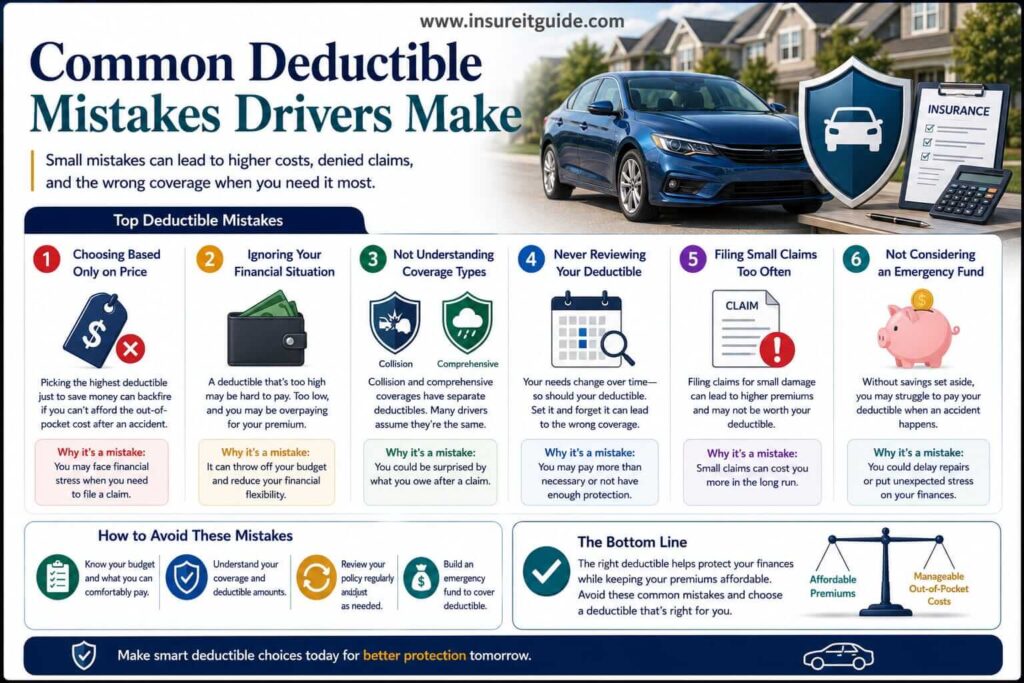

Common Insurance Deductible Mistakes

Many drivers accidentally make expensive deductible mistakes.

Choosing a Deductible That Is Too High

Some drivers lower premiums aggressively without considering whether they could realistically afford the deductible later.

Choosing a Deductible Based Only on Monthly Cost

Insurance decisions should involve overall financial protection, not just premium savings.

Filing Very Small Claims

Small claims may provide limited financial benefit while potentially affecting future premiums.

Ignoring Policy Reviews

Vehicle value and financial situations change over time.

Deductibles should be reviewed periodically.

Assuming Deductibles Apply to Liability Claims

Liability insurance usually does not involve deductibles because it protects other people.

Understanding these mistakes helps drivers make smarter long-term insurance decisions.

Ways to Save Money Without Choosing a Risky Deductible

Drivers do not always need extremely high deductibles to reduce insurance costs.

Several safer strategies may help lower premiums.

Compare Insurance Quotes

Pricing varies significantly between insurers.

Shopping around regularly can often save hundreds of dollars annually.

Maintain a Clean Driving Record

Safe drivers generally receive lower premiums.

Bundle Insurance Policies

Many insurers offer discounts for combining:

- Auto insurance

- Home insurance

- Renters’ insurance

Ask About Discounts

Potential discounts include:

- Good student discounts

- Defensive driving discounts

- Multi-vehicle discounts

- Low-mileage discounts

- Military discounts

Improve Credit Score

In many states, credit-based insurance scores affect premiums.

Improving credit may reduce insurance costs.

These strategies may help lower premiums without creating dangerous out-of-pocket financial risk.

Frequently Asked Questions

What is an insurance deductible?

An insurance deductible is the amount you pay out of pocket before your insurer helps cover claim costs.

How does an insurance deductible work after an accident?

You pay the deductible amount first, and the insurer pays the remaining eligible covered costs.

Do you pay a deductible if the accident was not your fault?

Sometimes yes initially, but you may later recover the deductible if the at-fault insurer reimburses your company.

Is a higher deductible better for car insurance?

Higher deductibles usually lower premiums but increase out-of-pocket financial risk after claims.

What happens if damage costs less than the deductible?

Insurance generally does not pay anything if repair costs are below the deductible amount.

Does liability insurance have a deductible?

Liability insurance usually does not involve deductibles because it protects other people.

What deductible amounts are common?

Common deductibles include:

- $250

- $500

- $1,000

Should comprehensive and collision deductibles be different?

Yes. Many drivers choose different deductibles based on claim frequency and financial preference.

Key Takeaways

- An insurance deductible is the amount you pay before insurance coverage begins.

- Higher deductibles usually reduce premiums.

- Lower deductibles generally increase monthly insurance costs.

- Collision and comprehensive coverages usually include deductibles.

- Liability insurance typically does not involve deductibles.

- Choosing the right deductible depends on financial stability and risk tolerance.

- Drivers should avoid choosing deductibles they cannot comfortably afford.

- Understanding deductibles helps drivers make smarter insurance decisions.

Final Thoughts

Understanding insurance deductibles is one of the most important parts of choosing the right auto insurance policy.

Deductibles directly affect both:

- Monthly insurance costs

- Out-of-pocket financial risk

Choosing the right balance can help drivers avoid unnecessary financial stress after accidents.

The best deductible depends on:

- Emergency savings

- Vehicle value

- Driving habits

- Financial comfort level

- Long-term budget stability

Insurance decisions should never focus only on the cheapest monthly premium.

The goal should always be balancing affordability with meaningful financial protection.

Before adjusting your deductible, carefully evaluate whether you could realistically afford that amount after a serious accident.

The right insurance strategy should help protect your finances, not create additional financial hardship during stressful situations.

For more beginner-friendly insurance guides, educational financial content, and practical coverage comparisons, visit www.insureitguide.com.