Buying auto insurance can feel confusing, especially when policies include terms most drivers rarely hear outside the insurance world.

Collision coverage.

Comprehensive coverage.

Deductibles.

Full coverage.

Actual cash value.

For many drivers, these phrases blur together.

That confusion becomes a problem after an accident.

A driver might assume their insurance covers storm damage only to discover they never purchased comprehensive coverage. Another driver may believe a deer collision falls under collision insurance when it actually falls under comprehensive coverage.

These misunderstandings happen every day.

And they can become expensive.

Modern vehicles cost far more to repair than they did even a decade ago. Today’s cars contain advanced safety systems, radar sensors, cameras, lane-assist technology, adaptive cruise control systems, and expensive electronic components. Even relatively small accidents can generate repair bills worth thousands of dollars.

At the same time, weather-related vehicle damage is increasing across the United States.

Hurricanes.

Flooding.

Hailstorms.

Wildfires.

Theft.

Falling tree branches.

All of these risks have made understanding auto insurance coverage more important than ever.

That is why drivers frequently ask the following:

- What is the difference between collision and comprehensive coverage?

- Do I need both coverages?

- Does collision insurance cover hitting a deer?

- Is comprehensive insurance worth it for older cars?

- When should drivers drop collision coverage?

The answer depends on several factors, including your vehicle value, financial situation, driving habits, location, and risk tolerance.

In this complete guide, you will learn:

- What collision coverage protects

- What comprehensive insurance covers

- The biggest differences between both coverages

- Real-world examples of claims

- When each coverage makes sense

- How deductibles work

- Whether full coverage is worth it

- How lenders influence coverage requirements

- Ways to reduce insurance costs

- Common mistakes drivers make

By the end of this article, you will clearly understand collision vs. comprehensive coverage and how to choose protection that fits your financial situation.

Table of Contents

- What Is Collision Coverage?

- What Is Comprehensive Coverage?

- Collision vs Comprehensive Coverage: The Biggest Differences

- What Does Collision Coverage Cover?

- What Does Comprehensive Insurance Cover?

- What Collision Coverage Does NOT Cover

- What Comprehensive Coverage Does NOT Cover

- Does Collision Insurance Cover Hitting a Deer?

- How Deductibles Work for Collision and Comprehensive Coverage

- Collision vs Comprehensive Coverage Cost Comparison

- Do You Need Collision and Comprehensive Coverage?

- When Should Drivers Drop Collision Coverage?

- Is Comprehensive Coverage Worth It for Older Cars?

- Collision vs Comprehensive Coverage for Financed and Leased Vehicles

- Common Mistakes Drivers Make With Full Coverage Insurance

- Ways to Save Money on Collision and Comprehensive Insurance

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

What Is Collision Coverage?

Collision coverage is a type of auto insurance that helps pay to repair or replace your vehicle after an accident involving a collision.

Unlike liability insurance, which mainly protects other people, collision coverage protects your own vehicle.

Collision insurance typically applies when your car is damaged after the following:

- Hitting another vehicle

- Hitting a pole

- Crashing into a fence

- Striking a guardrail

- Rolling over

- Backing into an object

- Single-car accidents

For example, imagine sliding on a wet road and crashing into a concrete barrier.

Even though no other driver was involved, your vehicle still suffered damage from a collision.

Collision insurance may help pay for:

- Vehicle repairs

- Replacement costs if the car is totaled

- Damage caused by rollover accidents

This is one reason collision coverage is especially important for newer vehicles.

Repairing modern vehicles is increasingly expensive because cars now contain advanced safety systems and electronic components.

Even a damaged bumper can involve the following:

- Radar sensors

- Parking cameras

- Blind-spot monitoring systems

- Expensive electronics

- Calibration procedures

A relatively small accident may generate repair bills worth several thousand dollars.

Without collision coverage, drivers may need to pay those costs entirely out of pocket.

That financial risk becomes especially important for:

- New car owners

- Drivers with financed vehicles

- Families relying heavily on one vehicle

- Commuters driving daily

Collision insurance helps reduce that financial exposure.

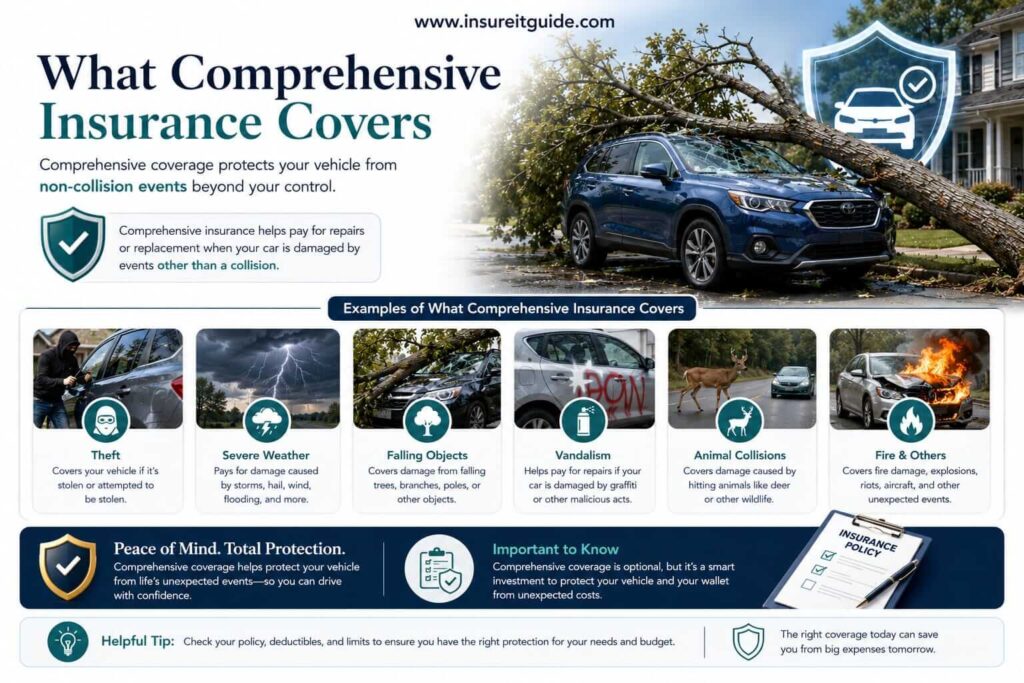

What Is Comprehensive Coverage?

Comprehensive coverage protects your vehicle from non-collision damage.

In simple terms, comprehensive insurance covers events that are usually outside your direct control.

This may include:

- Theft

- Hail damage

- Flood damage

- Fire

- Falling tree branches

- Vandalism

- Storm damage

- Animal collisions

- Broken windshields

- Natural disasters

For example, imagine your car is parked outside during a severe hailstorm.

The storm damages the hood, roof, and windshield.

Because the damage did not come from a driving collision, collision insurance would generally not apply.

Comprehensive insurance may help cover those repair costs.

Now imagine another situation.

You wake up in the morning and discover your vehicle was stolen overnight.

Again, this is not a collision-related event.

Comprehensive coverage may help reimburse the vehicle’s value.

Comprehensive insurance becomes especially valuable in areas exposed to:

- Severe weather

- Hurricanes

- Flooding

- Wildfires

- High theft rates

- Heavy deer populations

Many drivers underestimate how common non-collision vehicle damage actually is.

Across the United States, weather-related vehicle claims continue increasing every year.

In many regions, comprehensive insurance protects against risks drivers face far more often than major crashes.

That is why comprehensive coverage is considered one of the most valuable optional protections in modern auto insurance policies.

Collision vs Comprehensive Coverage: The Biggest Differences

Drivers often confuse collision and comprehensive coverage because both help protect their own vehicle.

However, they protect against very different risks.

Here is the simplest way to understand the difference:

Collision Coverage

Collision coverage protects against damage caused by driving collisions.

Comprehensive Coverage

Comprehensive coverage protects against non-collision events.

The distinction sounds simple, but real-world claims can sometimes confuse drivers.

Here is a quick comparison table.

| Coverage Type | Typically Covers |

| Collision Coverage | Crashes involving vehicles or objects |

| Comprehensive Coverage | Theft, storms, fire, vandalism, animal damage |

Collision Examples

Collision coverage may apply after the following:

- Rear-ending another vehicle

- Hitting a mailbox

- Sliding into a guardrail

- Backing into a pole

- Single-vehicle rollover accidents

Comprehensive Examples

Comprehensive coverage may apply after:

- Hailstorms

- Flooding

- Theft

- Fire damage

- Falling trees

- Animal collisions

- Broken windshields

Understanding this difference helps drivers avoid one of the biggest insurance mistakes:

assuming “full coverage” automatically means every type of damage is covered equally.

Insurance policies still contain:

- Exclusions

- Deductibles

- Coverage limits

- Claim conditions

That is why reviewing your policy carefully matters.

What Does Collision Coverage Cover?

Collision insurance helps repair or replace your vehicle after accidents involving impact or collisions.

Coverage may include:

- Damage from hitting another vehicle

- Single-car accidents

- Damage from hitting stationary objects

- Rollover accidents

- Damage caused by potholes in some situations

Collision coverage generally applies regardless of fault.

For example, if you accidentally hit another car at an intersection, your collision coverage may help repair your own vehicle even if you caused the accident.

This becomes especially important because modern repair costs can become extremely expensive.

Today’s vehicles often require the following:

- Sensor recalibration

- Camera replacement

- Advanced diagnostics

- Specialized labor

- Expensive electronic repairs

Even a damaged bumper may involve thousands of dollars in repairs.

Collision insurance can help drivers avoid paying those costs entirely out of pocket.

When Collision Coverage Is Most Valuable

Collision coverage is often most valuable for

- New vehicles

- Financed cars

- Leased vehicles

- High-value cars

- Drivers with long commutes

- Families relying heavily on one vehicle

If replacing or repairing your vehicle would create serious financial hardship, collision coverage may provide valuable protection.

What Does Comprehensive Insurance Cover?

Comprehensive insurance protects against non-collision vehicle damage.

Coverage may include:

- Theft

- Vandalism

- Hail damage

- Flooding

- Fire damage

- Falling objects

- Windstorm damage

- Animal collisions

- Broken glass

- Natural disasters

Comprehensive insurance is especially valuable because many non-collision events are completely outside the driver’s control.

For example:

- A tree branch falls during a storm

- Hail damages your vehicle overnight

- A flood destroys your parked car

- Your windshield cracks from flying debris

- Your car is stolen from a parking lot

None of these situations involve a driving collision.

That is why comprehensive insurance exists.

Weather-related claims are increasing.

Across the United States, severe weather events continue increasing.

Drivers now face growing risks from:

- Hurricanes

- Wildfires

- Hailstorms

- Flooding

- Tornadoes

- Severe winter storms

Comprehensive insurance may become especially important in regions prone to these risks.

Animal Collisions

Many drivers are surprised to learn animal collisions usually fall under comprehensive coverage rather than collision coverage.

For example:

- Hitting a deer

- Striking livestock

- Animal-related roadway damage

These incidents are generally treated as non-collision claims.

This distinction becomes important because comprehensive claims sometimes affect insurance premiums differently than at-fault collision claims.

What Collision Coverage Does NOT Cover

Collision insurance protects against accidents involving impact or collisions.

However, many drivers misunderstand what collision insurance excludes.

Collision coverage usually does NOT cover:

- Theft

- Flood damage

- Fire damage

- Hail damage

- Vandalism

- Falling objects

- Animal collisions

- Mechanical breakdowns

- Wear and tear

For example, if your car is damaged during a hurricane flood, collision coverage generally would not apply.

Likewise, if someone steals your vehicle, collision insurance would not typically help reimburse the loss.

Drivers often discover these limitations only after filing claims.

That is why understanding coverage exclusions matters just as much as understanding what policies include.

What Comprehensive Coverage Does NOT Cover

Although comprehensive insurance covers many non-collision risks, it still has important limitations.

Comprehensive insurance usually does NOT cover:

- Collision accidents

- Damage from hitting another vehicle

- Normal wear and tear

- Mechanical failures

- Engine breakdowns

- Tire damage from normal use

- Personal belongings inside the car

For example, if your transmission fails because of mechanical problems, comprehensive coverage generally would not pay for repairs.

Similarly, if you accidentally crash into another vehicle, collision coverage, not comprehensive coverage, would typically apply.

This distinction explains why many drivers purchase both collision and comprehensive insurance together.

Each coverage protects against different risks.

Together, they provide broader vehicle protection.

Does Collision Insurance Cover Hitting a Deer?

This is one of the most commonly misunderstood auto insurance questions.

Most animal collisions are generally covered under comprehensive insurance, not collision insurance.

For example, imagine driving on a dark rural highway when a deer suddenly runs into the road.

You hit the animal, damaging:

- The front bumper

- Headlights

- Hood

- Windshield

Even though your vehicle physically collided with something, insurers usually classify animal strikes as comprehensive claims.

Why?

Because the damage came from an unexpected non-driving hazard rather than a standard roadway collision.

This distinction matters because:

- Deductibles may differ

- Premium impact may differ

- Claim classification matters

Animal collisions are surprisingly common across many U.S. states.

Drivers in rural areas or regions with heavy deer populations often benefit significantly from comprehensive coverage.

Without comprehensive insurance, drivers may need to pay expensive repair costs themselves.

Modern vehicles with advanced front-end technology can become extremely expensive to repair after animal collisions.

How Deductibles Work for Collision and Comprehensive Coverage

Both collision and comprehensive insurance usually include deductibles.

A deductible is the amount you pay out of pocket before insurance coverage begins.

For example:

- Repair cost: $4,000

- Deductible: $500

- Insurance payout: $3,500

Higher deductibles generally reduce monthly insurance premiums.

Lower deductibles usually increase premiums.

Many drivers choose different deductibles for:

- Collision coverage

- Comprehensive coverage

For example:

- $1,000 collision deductible

- $250 comprehensive deductible

Why?

Because comprehensive claims such as windshield damage or hail damage may happen more frequently.

Drivers sometimes prefer lower deductibles for those situations.

Choosing deductibles involves balancing the following:

- Monthly affordability

- Emergency savings

- Risk tolerance

A deductible should always be an amount you could realistically afford after a claim.

Choosing extremely high deductibles simply to reduce premiums can become financially stressful later.

Collision vs Comprehensive Coverage Cost Comparison

Collision coverage usually costs more than comprehensive coverage.

Why?

Because collision claims occur more frequently and often involve expensive repairs.

Several factors influence pricing:

- Vehicle value

- Driving history

- Age

- Location

- Claim history

- Deductibles

- Traffic density

Comprehensive coverage is often relatively affordable compared to collision insurance.

Many drivers are surprised to learn they can add comprehensive coverage for a relatively modest increase in premiums.

This is especially true for:

- Older drivers with clean records

- Low-risk vehicles

- Areas with lower theft rates

However, costs vary significantly between insurance companies.

That is why comparing quotes remains one of the best ways to reduce insurance expenses.

Do You Need Collision and Comprehensive Coverage?

The answer depends on your financial situation and vehicle value.

Collision and comprehensive coverage are usually most valuable when

- Your vehicle is newer

- Your car still has high market value

- You rely heavily on the vehicle

- You could not comfortably replace the car yourself

- You live in high-risk weather areas

- Theft risk is high in your area

Drivers with financed or leased vehicles are often required to maintain both coverages.

Lenders want protection for the vehicle because technically they still hold financial interest in it.

When Both Coverages Make Sense

Many drivers benefit from carrying both collision and comprehensive insurance because together they protect against a wide range of risks.

This combination is commonly referred to as “full coverage,” although the term itself is not an official insurance product.

Full coverage usually includes the following:

- Liability insurance

- Collision coverage

- Comprehensive coverage

Without collision and comprehensive insurance, drivers may face major out-of-pocket expenses after accidents or weather-related damage.

When Should Drivers Drop Collision Coverage?

At some point, collision coverage may stop making financial sense.

This usually happens when:

- Vehicle value becomes very low

- Annual premiums remain high

- Potential claim payout becomes limited

For example, suppose the following:

- Your vehicle value: $3,500

- Collision deductible: $1,000

- Annual collision premium: $700

In this situation, the maximum practical payout may become relatively small.

Some drivers decide it makes more financial sense to save the premium money instead.

However, dropping collision coverage also increases personal financial risk.

Drivers should carefully evaluate the following:

- Vehicle replacement ability

- Emergency savings

- Dependence on the vehicle

- Overall financial situation

before removing coverage.

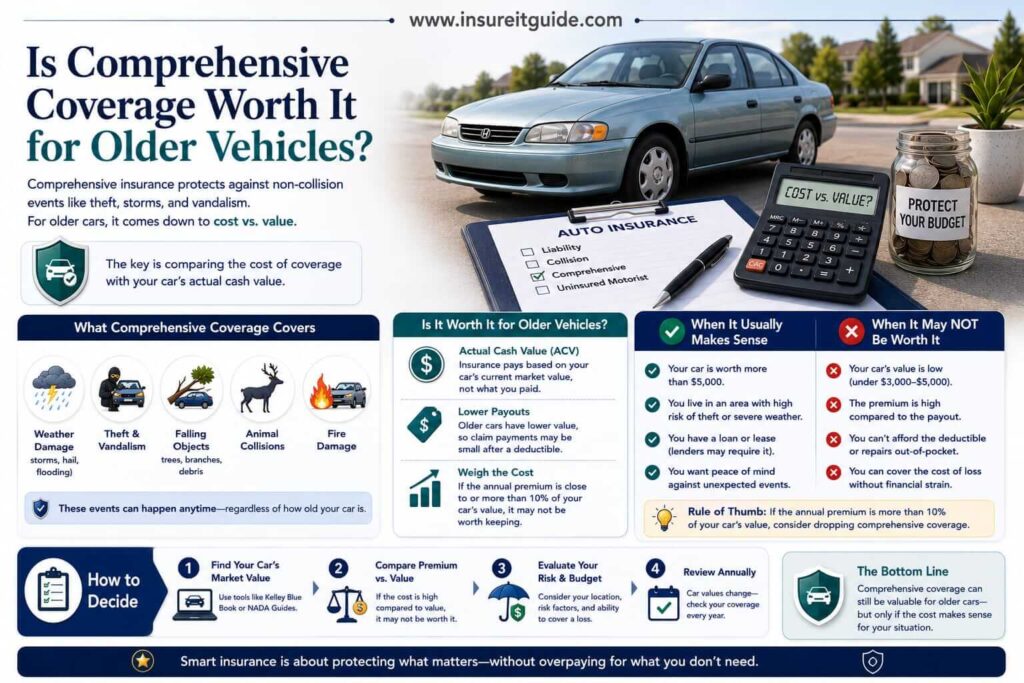

Is Comprehensive Coverage Worth It for Older Cars?

Comprehensive insurance often remains worthwhile even for older vehicles.

Why?

Because comprehensive coverage is usually cheaper than collision insurance while still protecting against:

- Theft

- Storm damage

- Hail damage

- Fire

- Falling objects

- Animal collisions

In some situations, keeping comprehensive coverage while dropping collision insurance can make financial sense.

For example:

- Older vehicle

- Moderate replacement value

- Low annual comprehensive premium

- High local theft risk

- Frequent severe weather

This strategy allows drivers to retain protection against unpredictable non-collision events without paying higher collision premiums.

Whether comprehensive insurance remains worthwhile depends heavily on:

- Vehicle value

- Local risks

- Insurance pricing

- Personal financial tolerance

Collision vs Comprehensive Coverage for Financed and Leased Vehicles

Drivers financing or leasing vehicles are usually required to carry the following:

- Collision coverage

- Comprehensive coverage

Why?

Because lenders and leasing companies want protection for the vehicle itself.

Until the loan is fully paid off, the lender still holds financial interest in the car.

If the vehicle is totaled, stolen, or severely damaged, the lender wants assurance the loss can be reimbursed.

Failing to maintain required coverage may result in:

- Force-placed insurance

- Higher costs

- Loan agreement violations

Force-placed insurance is often much more expensive and usually provides limited protection.

Drivers financing vehicles should carefully review lender insurance requirements before adjusting coverage.

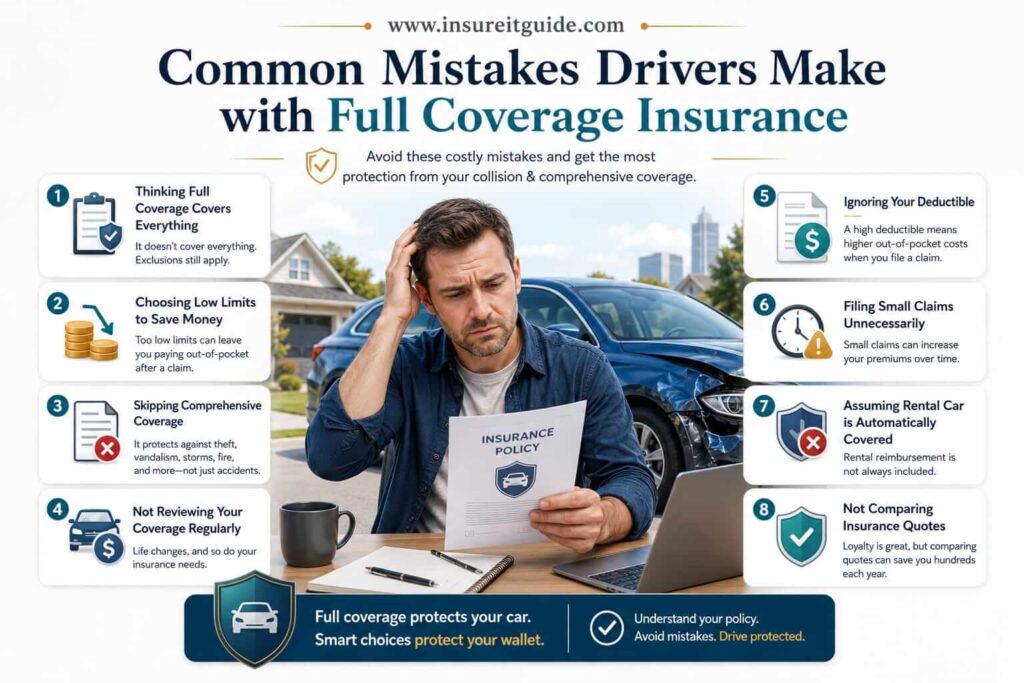

Common Mistakes Drivers Make With Full Coverage Insurance

Many drivers misunderstand what “full coverage” actually means.

Common mistakes include:

Assuming Everything Is Covered

Even full coverage policies contain exclusions.

Mechanical breakdowns, wear and tear, and certain damages may still not be covered.

Choosing Deductibles That Are Too High

Lower premiums can seem attractive until a claim happens.

Drivers should choose deductibles they could realistically afford.

Not Reviewing Vehicle Value

Older vehicles may no longer justify expensive collision coverage.

Ignoring Local Risk Factors

Drivers in areas prone to theft or severe weather may benefit significantly from comprehensive coverage.

Focusing Only on Monthly Premiums

The cheapest policy is not always the smartest financial choice.

Insurance decisions should balance:

- Affordability

- Protection

- Financial risk

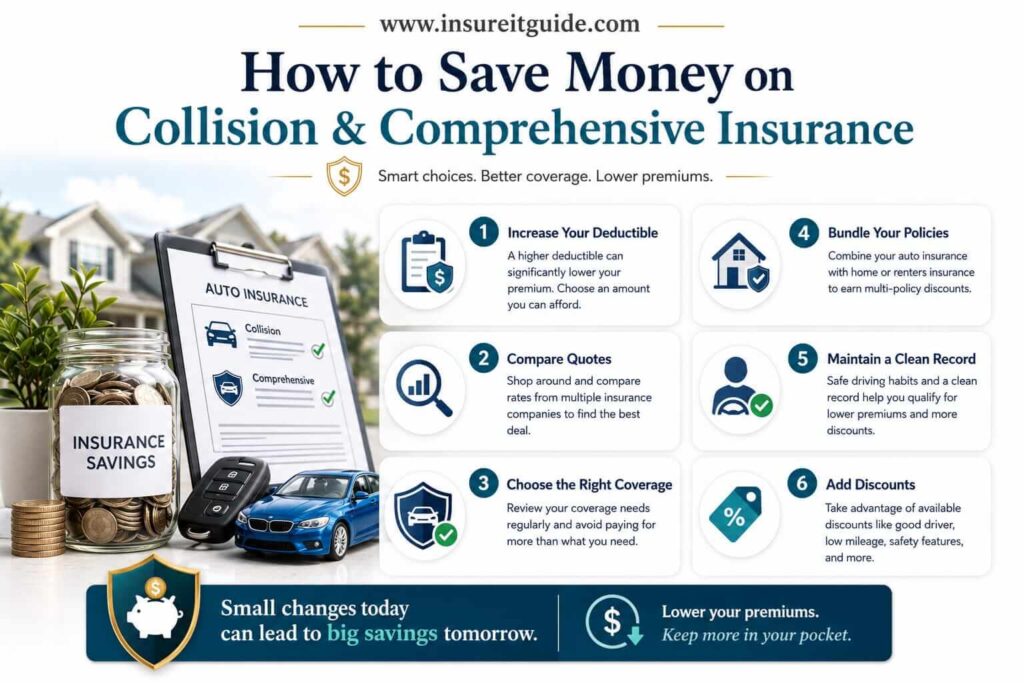

Ways to Save Money on Collision and Comprehensive Insurance

Auto insurance costs continue rising across the United States.

Fortunately, there are practical ways to reduce premiums without sacrificing important protection.

Compare Quotes Regularly

Rates vary significantly between insurers.

Comparing multiple quotes can often save hundreds of dollars annually.

Raise Deductibles Carefully

Higher deductibles usually lower premiums.

However, drivers should ensure deductibles remain affordable after claims.

Bundle Policies

Many insurers offer discounts for combining:

- Auto insurance

- Home insurance

- Renters’ insurance

Maintain a Clean Driving Record

Safe drivers generally receive lower premiums.

Ask About Discounts

Potential discounts include:

- Good student discounts

- Defensive driving discounts

- Low-mileage discounts

- Multi-car discounts

- Military discounts

Review Coverage Annually

Vehicle value changes over time.

Regular policy reviews help drivers avoid paying for unnecessary coverage.

Frequently Asked Questions

What is the difference between collision and comprehensive coverage?

Collision coverage protects against damage caused by driving collisions, while comprehensive coverage protects against non-collision events such as theft, storms, and vandalism.

Does collision insurance cover hitting a deer?

Usually no. Animal collisions are generally covered under comprehensive insurance.

Is comprehensive coverage worth it for older cars?

It often can be, especially in areas with severe weather or higher theft risk.

When should drivers drop collision coverage?

Drivers sometimes remove collision coverage when vehicle value becomes very low compared to premiums and deductibles.

Do financed vehicles require collision and comprehensive coverage?

Yes, lenders typically require both coverages until the loan is fully paid off.

What does comprehensive insurance cover after storms or theft?

Comprehensive insurance may help cover:

- Storm damage

- Hail damage

- Theft

- Fire

- Flooding

- Falling objects

What is a deductible?

A deductible is the amount you pay out of pocket before insurance coverage begins.

Key Takeaways

- Collision coverage protects against accident-related vehicle damage.

- Comprehensive coverage protects against non-collision risks.

- Animal collisions are usually covered under comprehensive insurance.

- Financed vehicles typically require both coverages.

- Deductibles affect both premiums and claim costs.

- Older vehicles may not always justify expensive collision coverage.

- Full coverage insurance generally combines liability, collision, and comprehensive protection.

- Comparing insurance quotes can help reduce costs significantly.

Final Thoughts

Understanding collision vs. comprehensive coverage is one of the most important parts of choosing the right auto insurance policy.

Both coverages protect your vehicle, but they protect against very different risks.

Collision coverage mainly protects against accident-related damage.

Comprehensive coverage protects against unpredictable non-collision events such as theft, storms, vandalism, and animal collisions.

The right combination depends on:

- Vehicle value

- Financial situation

- Driving habits

- Local weather risks

- Theft risk

- Personal financial tolerance

Choosing insurance should never be only about finding the cheapest premium.

It should be about protecting your financial future and reducing the risk of unexpected out-of-pocket expenses.

Before changing coverage, carefully review:

- Vehicle replacement value

- Deductibles

- Local risks

- Loan requirements

- Overall financial protection

For more beginner-friendly insurance guides, educational financial content, and practical auto insurance comparisons, visit www.insureitguide.com.