Buying car insurance sounds simple at first.

You pick a policy, pay your monthly premium, and assume you are protected if something goes wrong.

But after a real accident happens, many drivers discover they never fully understood what their insurance actually covered.

That confusion is especially common with liability insurance.

Some drivers think liability insurance pays for everything after a crash. Others assume it repairs their own vehicle automatically. Many people purchase only minimum state-required coverage without understanding how quickly accident expenses can exceed those limits.

Unfortunately, these misunderstandings can become financially devastating.

Medical bills in the United States are extremely expensive. Vehicle repair costs continue rising every year because modern cars contain advanced safety systems, cameras, sensors, and electronics. Even a moderate accident can generate repair costs worth thousands of dollars.

That is why understanding liability insurance coverage matters so much.

If you have ever asked:

- What does liability insurance cover?

- Does liability insurance cover my own car?

- What happens if damages exceed my policy limits?

- Is minimum liability coverage enough?

This complete guide will help you understand everything clearly.

In this detailed article, you will learn:

- What liability insurance actually covers

- What liability insurance does not cover

- How bodily injury liability works

- How property damage liability works

- The difference between liability and full coverage insurance

- How liability limits work

- Whether minimum coverage is enough

- How much liability insurance drivers may need

- Common insurance mistakes to avoid

- Smart ways to reduce insurance costs

By the end of this guide, you will understand how liability insurance works in real-world situations and how to choose protection that makes sense for your financial future.

Table of Contents

- What Is Liability Insurance?

- Why Liability Insurance Is Required in Most States

- What Does Liability Insurance Cover?

- Bodily Injury Liability Insurance Explained

- Property Damage Liability Coverage Explained

- What Liability Insurance Does Not Cover

- Liability vs Full Coverage Insurance

- How Liability Insurance Limits Work

- Minimum Liability Insurance Requirements by State

- What Happens If Damages Exceed Your Coverage Limits?

- How Much Liability Insurance Do You Need?

- Common Liability Insurance Mistakes Drivers Make

- Ways to Save Money on Liability Insurance

- Frequently Asked Questions

- Key Takeaways

- Final Thoughts

What Is Liability Insurance?

Liability insurance is a type of auto insurance that helps pay for injuries or property damage you cause to other people during a car accident.

In most states across the United States, liability insurance is legally required before drivers can operate vehicles on public roads.

The purpose of liability insurance is financial responsibility.

Car accidents can create extremely expensive financial losses. Without insurance laws, many accident victims would struggle to recover money for the following:

- Medical bills

- Vehicle repairs

- Property damage

- Lost wages

- Rehabilitation costs

- Legal claims

Liability insurance helps reduce that risk.

Most liability insurance policies contain two major parts:

- Bodily injury liability insurance

- Property damage liability coverage

Together, these coverages form the foundation of most basic auto insurance policies.

For example, imagine you accidentally rear-end another vehicle while driving through traffic.

The other driver suffers injuries, and their vehicle is heavily damaged.

Your liability insurance may help pay for:

- The injured driver’s medical expenses

- Their lost wages

- Their vehicle repair costs

- Legal claims related to the accident

However, liability insurance usually does not pay for damage to your own vehicle.

That is one of the biggest misunderstandings among drivers.

Many people buy liability-only insurance because it is cheaper than full coverage insurance. But they later discover their own vehicle repairs are not covered after an at-fault accident.

Understanding this distinction is extremely important when choosing insurance coverage.

Why Liability Insurance Is Required in Most States

Nearly every state requires drivers to carry liability insurance because accidents can create major financial consequences.

Without insurance requirements, accident victims might have no practical way to recover compensation after crashes.

Imagine a driver causing a serious multi-vehicle accident without insurance.

The accident could involve:

- Multiple injured drivers

- Emergency medical treatment

- Ambulance transportation

- Surgery expenses

- Vehicle replacement costs

- Property damage

- Lawsuits

Those costs can easily reach tens or even hundreds of thousands of dollars.

State governments require liability insurance to reduce financial harm after accidents and ensure drivers maintain at least some ability to compensate others.

However, every state regulates insurance differently.

That is why liability insurance requirements vary across the country.

Some states require only basic liability limits.

Others require:

- Personal Injury Protection (PIP)

- Uninsured motorist coverage

- Higher liability limits

- No-fault insurance systems

Several factors influence these laws:

Population Density

States with heavier traffic usually experience more accidents.

For example:

- California

- Texas

- Florida

- New York

all experience extremely high traffic volume.

More traffic generally means the following:

- Higher accident frequency

- Larger claim costs

- More lawsuits

Medical Costs

Healthcare expenses vary significantly across states.

Areas with higher medical costs often require stronger insurance protections.

Weather Risks

Weather conditions influence accident risks heavily.

Examples include:

- Florida hurricanes

- Northern snowstorms

- Colorado hail damage

- California wildfire risks

Legal Systems

Some states experience more litigation after accidents, which increases insurance costs and influences liability laws.

Because of these differences, insurance requirements vary considerably across the United States.

What Does Liability Insurance Cover?

Liability insurance generally covers financial losses suffered by other people when you are legally responsible for causing an accident.

Coverage may include:

- Emergency medical treatment

- Hospital bills

- Ambulance transportation

- Surgical procedures

- Rehabilitation expenses

- Lost wages

- Property damage

- Vehicle repair costs

- Legal defense expenses

- Court settlements

- Pain and suffering claims

The exact coverage depends on:

- Your insurance policy

- State laws

- Coverage limits

- Accident circumstances

Liability insurance becomes especially important after serious accidents involving:

- Multiple vehicles

- Expensive cars

- Injuries

- Property damage

- Lawsuits

Modern accidents are increasingly expensive.

Today’s vehicles contain:

- Radar systems

- Backup cameras

- Lane-assist technology

- Expensive electronics

- Advanced sensors

Even relatively small collisions can generate repair bills worth thousands of dollars.

Medical costs can become even more expensive.

A short emergency room visit combined with ambulance transportation and imaging scans can quickly exceed low liability limits.

This is why many financial professionals recommend liability limits significantly above state minimum requirements.

Liability insurance protects drivers from potentially devastating financial consequences.

Without adequate coverage, drivers may face:

- Lawsuits

- Wage garnishment

- Asset seizure

- Long-term debt

That is why understanding liability coverage is about much more than simply staying legal.

It is about protecting your financial future.

Bodily Injury Liability Insurance Explained

Bodily injury liability insurance helps pay for injuries suffered by other people when you cause an accident.

This coverage may help pay for:

- Emergency room treatment

- Hospital stays

- Surgical procedures

- Rehabilitation therapy

- Physical therapy

- Lost wages

- Disability-related costs

- Legal settlements

- Funeral expenses in severe accidents

Medical expenses in the United States can become extremely expensive very quickly.

That is why bodily injury liability coverage is one of the most important parts of an auto insurance policy.

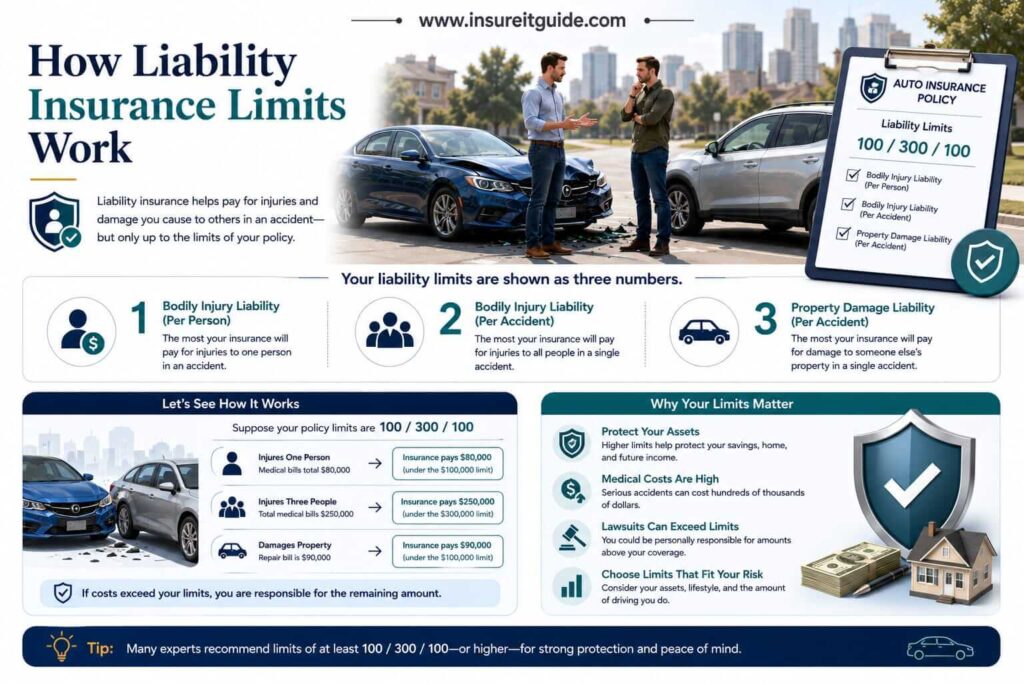

Most insurers display liability limits using three numbers.

Example:

25/50/25

This usually means:

- $25,000 bodily injury coverage per person

- $50,000 bodily injury coverage per accident

- $25,000 property damage coverage

Imagine you cause an accident involving two injured drivers.

Driver A’s medical bills: $20,000

Driver B medical bills: $45,000

If your bodily injury coverage limit is 25/50/25:

- Your insurer may pay up to $25,000 for Driver B

- The remaining balance could become your responsibility

This is why low liability limits can create serious financial risk.

Many drivers mistakenly believe state minimum coverage automatically provides sufficient protection.

In reality, one major accident can exceed low policy limits surprisingly quickly.

That is especially true today because

- Healthcare inflation continues rising

- Surgeries are expensive

- Rehabilitation costs are increasing

- Long-term treatment can become extremely costly

Drivers with families, savings, homes, or investments often choose higher liability limits to reduce financial exposure after serious accidents.

Property Damage Liability Coverage Explained

Property damage liability coverage helps pay for damage you cause to another person’s property during an accident.

Examples include:

- Vehicle repair costs

- Totaled vehicle replacement

- Fence damage

- Garage repairs

- Building damage

- Utility pole repairs

- Street sign replacement

- Public property damage

Property damage claims are becoming increasingly expensive because modern vehicles cost far more to repair than older vehicles.

Today’s cars often contain the following:

- Cameras

- Radar systems

- Adaptive cruise control systems

- Blind-spot sensors

- Expensive computer systems

Even relatively minor accidents can require costly recalibration procedures and specialized repairs.

Luxury vehicles and electric vehicles can generate especially expensive repair claims.

For example, damaging the front bumper of a newer luxury SUV may involve:

- Sensor replacement

- Camera recalibration

- Electronic system diagnostics

- Specialized labor

Repair costs can quickly exceed several thousand dollars.

This is one reason financial professionals often recommend stronger property damage liability coverage than state minimum requirements.

Low property damage limits can leave drivers financially exposed after accidents involving:

- Expensive vehicles

- Commercial property

- Multiple vehicles

- Public infrastructure

Choosing stronger liability protection may help reduce long-term financial risk.

What Liability Insurance Does Not Cover

One of the biggest insurance misunderstandings among drivers is assuming liability insurance covers everything after an accident.

It does not.

Liability insurance usually does NOT cover:

- Damage to your own vehicle

- Your own medical expenses

- Theft

- Vandalism

- Flood damage

- Fire damage

- Hail damage

- Falling objects

- Animal collisions

To receive protection for your own vehicle, you typically need additional coverages such as the following:

- Collision coverage

- Comprehensive coverage

- Personal Injury Protection (PIP)

- Medical Payments coverage

For example, suppose you accidentally hit another vehicle.

Your liability insurance may help pay for the other driver’s vehicle repairs and medical expenses.

However, your own vehicle repairs may not be covered unless you also carry collision insurance.

This distinction becomes extremely important after expensive accidents.

Many drivers discover too late that liability-only insurance leaves major gaps in protection.

That is why drivers should carefully evaluate the following:

- Vehicle value

- Financial situation

- Driving habits

- Risk tolerance

before choosing liability-only coverage.

Liability vs Full Coverage Insurance

Many drivers confuse liability insurance with full coverage insurance.

These are not the same thing.

Liability Insurance

Liability insurance primarily protects other people when you cause accidents.

It generally includes:

- Bodily injury liability

- Property damage liability

Full Coverage Insurance

Full coverage insurance usually includes the following:

- Liability insurance

- Collision coverage

- Comprehensive coverage

Collision coverage helps repair your own vehicle after accidents.

Comprehensive insurance covers non-collision damage such as

- Theft

- Flooding

- Fire

- Hail

- Falling objects

- Vandalism

- Animal collisions

Drivers with financed or leased vehicles are often required by lenders to maintain full coverage insurance because lenders want protection for the vehicle itself.

Although full coverage costs more, it usually provides much broader financial protection.

Whether full coverage makes sense depends on:

- Vehicle value

- Financial situation

- Driving habits

- Risk tolerance

Drivers with newer vehicles often prefer stronger coverage because repair or replacement costs may be substantial.

How Liability Insurance Limits Work

Liability insurance policies contain maximum payout limits.

Example:

100/300/100

This usually means:

- $100,000 bodily injury coverage per person

- $300,000 bodily injury coverage per accident

- $100,000 property damage coverage

Higher liability limits generally provide stronger financial protection.

However, higher limits also increase premiums.

Many financial professionals recommend higher liability limits for drivers who:

- Own homes

- Have savings or investments

- Drive frequently

- Commute long distances

- Live in high-traffic areas

- Have families

Imagine causing a major multi-vehicle accident involving injuries.

Medical costs and legal settlements can quickly exceed low liability limits.

Without adequate coverage, drivers may face lawsuits and major financial consequences.

That is why liability limits are one of the most important parts of an insurance policy.

Choosing the cheapest policy without evaluating liability limits can become extremely expensive later.

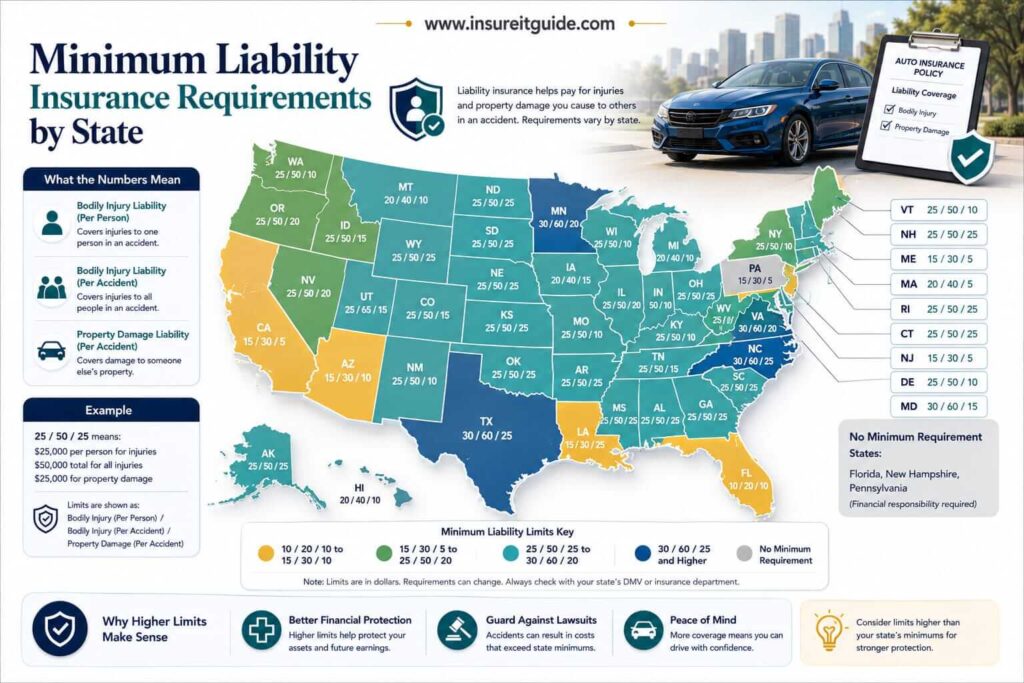

Minimum Liability Insurance Requirements by State

Every state sets its own minimum liability insurance requirements.

Examples include:

| State | Minimum Liability Limits |

| California | 15/30/5 |

| Texas | 30/60/25 |

| Florida | 10/20/10 |

| New York | 25/50/10 |

| Arizona | 25/50/15 |

| Nevada | 25/50/20 |

These numbers represent the minimum amount of liability insurance drivers must carry legally.

However, state minimum requirements are not necessarily sufficient financial protection.

A serious accident involving:

- Injuries

- Multiple vehicles

- Luxury cars

- Lawsuits

can easily exceed minimum limits.

That is why many drivers choose higher coverage levels than state law requires.

Drivers moving between states should also review insurance laws carefully because requirements vary considerably.

Whenever relocating, drivers should:

- Contact their insurer

- Review state laws

- Verify liability limits

- Update policy information

Failing to update coverage correctly may create legal or financial problems.

What Happens If Damages Exceed Your Coverage Limits?

If accident damages exceed your liability insurance limits, you may become personally responsible for the remaining amount.

This can lead to:

- Lawsuits

- Wage garnishment

- Asset seizure

- Financial hardship

- Long-term debt

For example:

- Your policy limit: $50,000

- Total damages: $150,000

- Remaining balance: $100,000

You could potentially owe the remaining balance personally.

This is why low liability limits can create serious financial exposure.

Many drivers mistakenly believe severe accidents are rare.

However, major accidents happen every day.

Modern healthcare costs and vehicle repair costs continue increasing, making stronger liability protection increasingly important.

Drivers with homes, savings, or investments often choose higher liability limits to help protect their financial future.

How Much Liability Insurance Do You Need?

The right amount of liability insurance depends on several personal factors.

These include:

- Income

- Savings

- Vehicle value

- Driving frequency

- State laws

- Family responsibilities

- Financial assets

Drivers with greater financial assets often choose higher liability protection because lawsuits after major accidents can threaten long-term financial stability.

Many insurance professionals recommend:

- Higher liability limits

- Moderate deductibles

- Uninsured motorist protection

- Collision and comprehensive coverage when appropriate

The cheapest policy is not always the smartest financial decision.

A balanced insurance strategy focuses on:

- Affordability

- Protection

- Long-term financial security

Choosing stronger liability protection may cost more monthly, but it can potentially prevent devastating financial losses after severe accidents.

Common Liability Insurance Mistakes Drivers Make

Many drivers accidentally make expensive insurance mistakes.

Choosing Coverage Based Only on Price

The cheapest policy often provides the least protection.

Low premiums may come with dangerously low liability limits.

Assuming Minimum Coverage Is Enough

State minimums satisfy legal requirements but may not fully protect drivers financially.

Not Reviewing Policies Regularly

Major life changes may require stronger protection.

Examples include:

- Marriage

- Buying a home

- Purchasing a new vehicle

- Relocating

- Having children

Ignoring Deductibles

Some drivers choose deductibles they cannot realistically afford after accidents.

Skipping Uninsured Motorist Coverage

Millions of drivers across the United States remain uninsured or underinsured.

This coverage can provide extremely valuable protection.

Reviewing insurance policies annually can help drivers avoid dangerous coverage gaps.

Ways to Save Money on Liability Insurance

Car insurance can become expensive, especially for younger drivers and families.

Fortunately, there are several practical ways to reduce premiums without sacrificing important protection.

Compare Quotes

Insurance rates vary significantly between companies.

Comparing multiple quotes can often save hundreds of dollars annually.

Maintain a Clean Driving Record

Safe drivers generally receive lower premiums.

Avoiding accidents and traffic violations can reduce insurance costs substantially over time.

Bundle Insurance Policies

Many insurers offer discounts for bundling:

- Auto insurance

- Home insurance

- Renters’ insurance

Increase Deductibles Carefully

Higher deductibles usually lower monthly premiums.

However, drivers should ensure they can realistically afford the deductible after accidents.

Ask About Discounts

Potential discounts include the following:

- Good student discounts

- Defensive driving discounts

- Military discounts

- Low-mileage discounts

- Multi-vehicle discounts

Improve Credit Score

In many states, insurers use credit-based insurance scores.

Improving credit may help reduce premiums.

Shopping around regularly remains one of the most effective ways to reduce insurance costs.

Frequently Asked Questions

What does liability insurance cover after a car accident?

Liability insurance generally covers injuries and property damage suffered by other people if you caused the accident.

Does liability insurance cover my own vehicle?

No. Liability insurance usually does not pay for repairs to your own vehicle.

What is bodily injury liability insurance?

It helps pay medical expenses and related losses for people injured in accidents you cause.

What is property damage liability coverage?

It helps pay for damage you cause to another person’s property during accidents.

Is minimum liability insurance enough?

Minimum coverage satisfies legal requirements but may not provide enough financial protection after serious accidents.

What happens if damages exceed my liability limits?

You may become personally responsible for remaining costs.

Is liability insurance required in every state?

Almost every U.S. state requires liability insurance or proof of financial responsibility.

Key Takeaways

- Liability insurance protects other people after accidents you cause.

- It usually includes bodily injury and property damage coverage.

- Liability insurance generally does not cover your own vehicle repairs.

- Full coverage insurance provides broader protection.

- State minimum limits may not fully protect drivers financially.

- Higher liability limits often provide stronger protection.

- Understanding policy limits is essential for financial safety.

- Comparing insurance quotes can help drivers save money.

Suggested Internal Links

| Suggested Anchor Text | Suggested Internal Link Topic |

| What is full coverage insurance? | Full coverage insurance guide |

| Collision vs comprehensive coverage | Coverage comparison article |

| Cheapest car insurance companies | Budget insurance guide |

| How car insurance deductibles work | Deductible explanation guide |

| Minimum car insurance requirements by state | State insurance laws guide |

Suggested External Authority References

- National Association of Insurance Commissioners (NAIC)

- Insurance Information Institute (III)

- USA.gov Insurance Resources

Final Thoughts

Understanding what liability insurance covers is one of the most important parts of becoming a financially responsible driver in the United States.

Liability coverage plays a critical role in protecting drivers from potentially devastating financial losses after accidents.

However, many drivers mistakenly assume minimum coverage protects everything, only to discover expensive coverage gaps after serious crashes.

The smartest insurance decisions come from understanding both

- What your policy covers

- What your policy does not cover

Before purchasing auto insurance, carefully review liability limits, compare coverage options, and evaluate whether stronger protection makes sense for your financial situation.

Choosing insurance should never be only about finding the cheapest premium.

It should be about protecting your finances, your family, and your long-term financial future.

For more beginner-friendly insurance guides, educational financial content, and practical coverage comparisons, visit www.insureitguide.com.